STRC preferred stock dividend hits 12% — every increase is permanent

0

0

Strategy’s STRC preferred stock dividend structure was always ambitious — a variable-rate instrument designed to fund one of the most aggressive Bitcoin accumulation programs in corporate history. But by late June 2026, STRC had dropped 25% below its $100 par value, the Rosen Law Firm had opened a legal investigation, and Strategy had made its first Bitcoin sale since 2022. The question now isn’t just how STRC works — it’s whether the mechanics that built it can hold it together.

Key takeaways

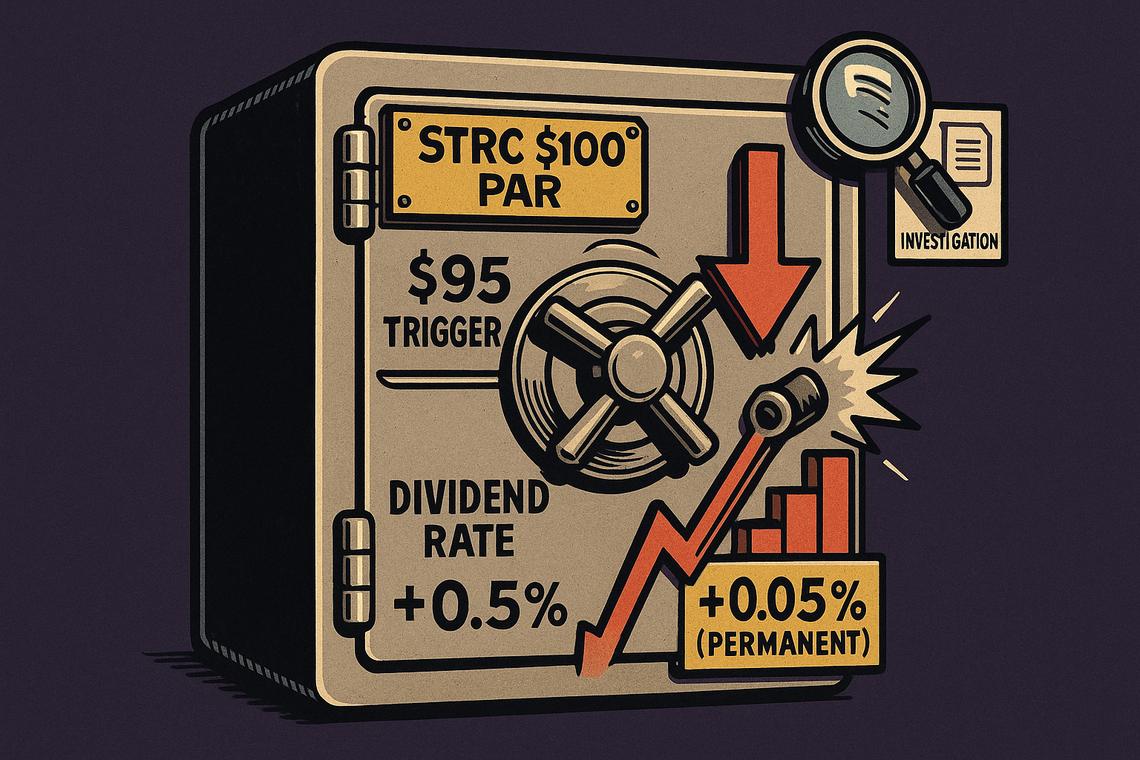

- STRC is Strategy’s perpetual preferred stock paying a variable dividend currently set at 12% annually, adjusted monthly by the board.

- Strategy held 847,363 Bitcoin as of early July 2026, funded partly through STRC issuance proceeds via at-the-market share sales.

- A dividend ratchet raises the rate by 0.5% increments each time STRC falls below $95 — permanently, even after Bitcoin recovers.

- Strategy maintains a $3.8 billion liquidity buffer — a $2.55 billion USD reserve plus $1.25 billion in Bitcoin monetization capacity — covering roughly 26 months of dividend obligations.

- Retail investors hold approximately 83% ($8.8 billion) of STRC, a concentration that JPMorgan and institutional analysts have flagged as a structural vulnerability.

Overview of STRC Preferred Stock and Dividend Mechanism

STRC — Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock — is a Nasdaq-listed instrument that pays semi-monthly cash dividends at a rate reviewed and reset every 30 days. The board uses a basket of inputs: STRC’s trading price, credit spreads, Bitcoin volatility, and USD reserve coverage. What it does not do is automatically raise the rate just because STRC trades below par — a distinction the June 29, 2026 8-K filing made explicit.

The rate launched at 9% in July 2025. It has risen seven consecutive times, reaching the current 12%. Each increase is permanent.

Variable Dividend Rate and Ratchet Mechanism

The ratchet is the sharpest edge in the instrument’s design. When STRC falls below $95, a contractual mechanism increases the dividend rate by 0.5 percentage point increments. JPMorgan analyst Nikolaos Panigirtzoglou estimated that each trigger adds roughly $53 million in annual obligations.

That asymmetry separates STRC from conventional preferred stocks. With a standard preferred, a price drop raises the effective yield for incoming buyers — but does nothing to the issuer’s cost structure. With STRC, the issuer’s obligations expand permanently. A Bitcoin recovery can return the share price to $100, but it cannot unwind a rate increase already locked in.

Onramp CEO Michael Tanguma put it plainly: “A capital structure that survives volatility only by adding permanent obligations is a structure with a finite number of cycles in it.”

Dividend Payment Terms and Adjustments

STRC dividends are cumulative — missed payments accrue and must be satisfied before any common stock distributions. Shareholders approved a shift to semi-monthly payments on June 8, 2026. Strategy CEO Phong Le described the change as designed to “stabilize price, dampen cyclicality, drive liquidity, and grow demand.”

The cumulative structure is significant. It means unpaid dividends do not disappear — they pile up as senior obligations ahead of common shareholders, adding another layer of pressure during prolonged Bitcoin drawdowns.

STRC Par Value Dynamics and Price Performance

Par value is the operational heartbeat of the entire STRC model. At $100, Strategy can sell new shares through its ATM program at roughly par, efficiently raising capital for Bitcoin purchases. That mechanism generated $5.6 billion in gross STRC proceeds through Q1 2026.

Significance of the $100 Par Value Anchor

When STRC trades at or near $100, the flywheel works cleanly: Strategy issues new shares, raises cash, buys Bitcoin, and the Bitcoin appreciation supports demand for more STRC. The $100 anchor is not just a price target — it is the condition under which the entire capital-raising engine functions.

Lose the anchor, and the machine stalls.

Price Decline and Impact on Dividend Obligations

Between mid-May and late June 2026, Bitcoin fell from above $80,000 to below $60,000. STRC followed, hitting a low of $71.25 before recovering to close at $87.87 on July 3. By June 20, STRC stood at $83 — 25% below par. During that window, Strategy used cash reserves to repurchase $1.5 billion in convertible notes and executed its first Bitcoin sale since 2022: 3,588 BTC sold for approximately $216 million, with proceeds used to fund preferred stock distributions and replenish the USD reserve to $2.55 billion.

The ratchet had already been triggered. With each trigger permanently embedded in the rate structure, the cost of the next drawdown compounds on top of the last one.

Strategy’s Bitcoin Holdings and Funding Structure

Strategy’s Bitcoin treasury is the underlying collateral that gives STRC its credibility — and its risk. As of early July 2026, the company held 847,363 Bitcoin, acquired at an average cost of approximately $74,476 per coin. At recent prices around $60,000, that position carried roughly $11.4 billion in paper losses.

Bitcoin Treasury Scale and Acquisition Funding

STRC was the primary engine of Bitcoin accumulation earlier in 2026. The model: issue STRC at or near par, convert proceeds to Bitcoin, let Bitcoin appreciation validate the cycle. The instrument raised $5.6 billion in gross proceeds through Q1 2026 alone.

That engine has been idle since mid-May. With STRC trading well below par, new issuance would dilute existing holders and raise capital at a discount — economically counterproductive. Strategy has essentially paused Bitcoin accumulation while it works to restore par.

Liquidity Buffer and Dividend Coverage

The newly announced Digital Credit Capital Framework requires the USD reserve to cover at least 12 months of preferred obligations at all times. As of July 5, that reserve stood at $2.55 billion. Add the $1.25 billion Bitcoin Monetization Program — which allows Strategy to sell Bitcoin specifically to fund dividends and repurchases — and total liquidity coverage reaches $3.8 billion, roughly 26 months of obligations.

CryptoQuant had noted that dividend coverage had collapsed from over seven years to about 14 months before the framework was introduced, recommending reserves be restored to $2.8 billion before Bitcoin accumulation resumed. The $2.55 billion figure suggests Strategy is close to that threshold but has not yet crossed it.

Separately, Strategy’s $1 billion Digital Credit Securities Repurchase Program — covering STRC, STRF, STRD, and STRK, with STRC as the initial priority — serves as the direct intervention tool for restoring par value. Share buybacks reduce supply in the market, supporting price.

Investor Composition and Market Risks

Retail Investor Concentration and Implications

The investor base tells a story that institutional analysts find uncomfortable. Retail investors hold an estimated $8.8 billion of STRC, approximately 83% of the buyer base. That concentration was flagged by JPMorgan as a structural concern — retail holders tend to be more reactive to sentiment shifts, creating the potential for sharp, self-reinforcing selloffs during drawdowns.

By contrast, institutional adoption is growing, if still modest: $150 million in STRC sits in corporate treasuries, and $270 million across DeFi protocols including Apyx and Saturn, per Strategy’s Q1 disclosures. The trajectory is positive, but the current composition leaves STRC exposed to retail panic in ways a more institutionally-held instrument would not be.

Bitcoin Price Volatility and Its Effects on STRC

Bitcoin’s price movement is not just background noise for STRC — it is the primary driver of nearly every risk in the structure. A falling Bitcoin price reduces STRC’s trading price, triggers the ratchet, raises annual obligations, potentially pushes Strategy toward Bitcoin sales that further weaken market confidence, and increases the cost of the next accumulation cycle.

JPMorgan also warned that Strategy’s willingness to sell Bitcoin — now demonstrated with the 3,588 BTC sale — turns the world’s largest institutional accumulator into a potential seller. That two-way dynamic changes the market psychology around Strategy’s Bitcoin position in ways that are difficult to quantify but hard to ignore.

Regulatory Environment and Legal Challenges

STRC is SEC-registered and Nasdaq-listed, giving it the institutional credibility of a regulated instrument. That regulatory standing also means legal exposure when performance falls short of investor expectations.

The Rosen Law Firm opened an investigation on June 25, 2026, examining whether Strategy can continue servicing preferred payments if Bitcoin remains below its average cost basis of approximately $75,651 per coin. The investigation does not represent a formal charge or finding, but it signals the kind of scrutiny that can weigh on investor sentiment — particularly for the retail-heavy holder base.

On the legislative front, the Clarity Act, if passed, could reclassify Bitcoin treasury companies for tax purposes. That reclassification might alter the return-of-capital treatment currently expected for STRC dividends — Strategy has indicated it expects STRC dividends to qualify as return of capital for U.S. tax purposes, reducing a holder’s cost basis rather than generating immediate ordinary taxable income. Any change to that treatment would directly affect the after-tax return calculation for millions of retail holders.

The August monthly dividend reset and the next quarterly earnings will be the first real test of whether the Digital Credit Capital Framework and the $1 billion repurchase program can put a floor under STRC. If Bitcoin stabilizes above $75,000 and the reserve holds, the flywheel can restart. If Bitcoin slides further, each new ratchet trigger will have been built on top of permanent obligations already accumulated through previous cycles — and the question Tanguma raised about finite cycles will feel considerably less rhetorical.

FAQ

What is STRC?

STRC is Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock, a Nasdaq-listed instrument paying semi-monthly cash dividends at a variable rate currently set at 12% annually.

How does STRC’s dividend rate get adjusted?

Strategy’s board reviews the rate monthly based on trading price, credit spreads, Bitcoin volatility, and USD reserve coverage, adjusting in increments of up to 0.25% per period. The rate does not automatically increase just because STRC trades below par.

What is the significance of STRC’s $100 par value?

STRC targets a $100 stated amount as its trading anchor. When STRC trades near par, Strategy can raise capital efficiently through at-the-market share sales to fund Bitcoin purchases. Below par, that capital-raising mechanism effectively shuts down.

What happens when STRC trades below $95?

A contractual ratchet increases the dividend rate by 0.5 percentage point increments, adding roughly $53 million in annual obligations per trigger. These increases are permanent — they do not reverse when the price recovers.

How does Strategy fund STRC dividend payments?

Dividends are funded through ATM share sales when STRC trades near par, software revenue generating roughly $320 million annually in gross profit, and the newly authorized $1.25 billion Bitcoin Monetization Program.

Article produced with the assistance of artificial intelligence and reviewed by the editorial team.

0

0

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.

0

0

0

0

0

0