0

0

NFTs are digital assets that represent ownership of unique content on a blockchain. Unlike regular digital files that can be copied endlessly, NFTs are designed to be one of a kind, which makes each asset valuable to creators and collectors. NFTs can represent art, music, videos, collectibles, and virtual items used in games or online communities.

In recent years, NFTs have created new opportunities for creators to earn directly from creative work without relying on traditional platforms. Understanding how NFTs are made is the first step toward exploring this space, whether the goal is creative expression, brand building, or income generation. This guide explains how to make NFTs step by step, from choosing a digital asset to minting and selling it on an NFT marketplace.

NFTs, short for non-fungible tokens, are digital assets that represent ownership of unique digital assets on a blockchain. Each NFT carries specific data that distinguishes one asset from another, even when multiple items look similar. This uniqueness prevents an NFT from being exchanged one-to-one for another asset of the same collection or type.

NFTs can represent digital art, music files, videos, collectibles, virtual land, game items, and written content. When an NFT is created, information such as the creator’s address, ownership history, and transaction records becomes permanently stored on the blockchain. This record allows anyone to verify authenticity and trace ownership from the original creator to the current owner.

Unlike traditional digital formats, NFTs (non-fungible tokens) cannot be duplicated in terms of ownership. Copies of the content may exist, but only one crypto wallet holds the verified token connected to the original asset. This structure gives creators a way to sell digital work with proof of originality and gives buyers confidence in the asset’s authenticity.

NFTs also support smart contracts, which allow creators to make money with NFTs via royalties whenever an asset is resold. This feature creates long-term value for creators beyond the first sale and introduces a new model for digital ownership and distribution. If you want to know more about NFTs, including how ownership works, their use cases, and examples in the real world.

The first step in creating a non-fungible token (NFT) is selecting the digital work/content to tokenize. This content must be original or something the creator owns full rights to use. NFTs work best when the asset has a clear purpose, story, or visual identity. Common digital assets used for NFTs include digital artwork, illustrations, photographs, music files, videos, animations, virtual items, and written content.

High-quality files often perform better, especially in marketplaces where presentation matters to buyers. Before moving forward, the asset should be finalized. Edits made after minting do not change the original NFT stored on the blockchain. Taking time to refine the asset helps avoid irreversible mistakes.

The blockchain determines how the NFT is created, stored, and traded. Each blockchain offers different benefits in terms of transaction fees, speed, security, and marketplace support. Ethereum remains the most widely used blockchain for NFTs, known for strong security and large marketplaces, though minting fees can be high.

Polygon offers lower fees and supports free or low-cost minting, making it popular among beginners. Solana provides fast transactions and low transaction costs, often used for gaming and large NFT collections. Tezos and BNB Chain also offer affordable alternatives with growing communities.

Choosing the right blockchain depends on budget, target audience, and long-term goals. Once selected, the non-fungible token becomes tied to that blockchain and cannot be moved without creating a new token.

A crypto wallet is required to store your NFTs and other crypto assets, as well as to interact with NFT marketplaces. Wallets provide the address used for minting and receiving payments. Choosing a secure wallet is essential, as losing access means losing NFTs permanently. Popular wallets include MetaMask, Trust Wallet, Binance Wallet, Base Wallet, Phantom, and Ledger for hardware storage.

When creating a wallet, a recovery phrase will be provided. This phrase must be stored safely offline and never shared, as it is the only way to recover access if the wallet is lost. Some blockchains require specific wallets. For example, Solana often uses Phantom, while the Ethereum blockchain works with MetaMask or Base Wallet. Ensure the wallet is compatible with the chosen blockchain and NFT marketplace.

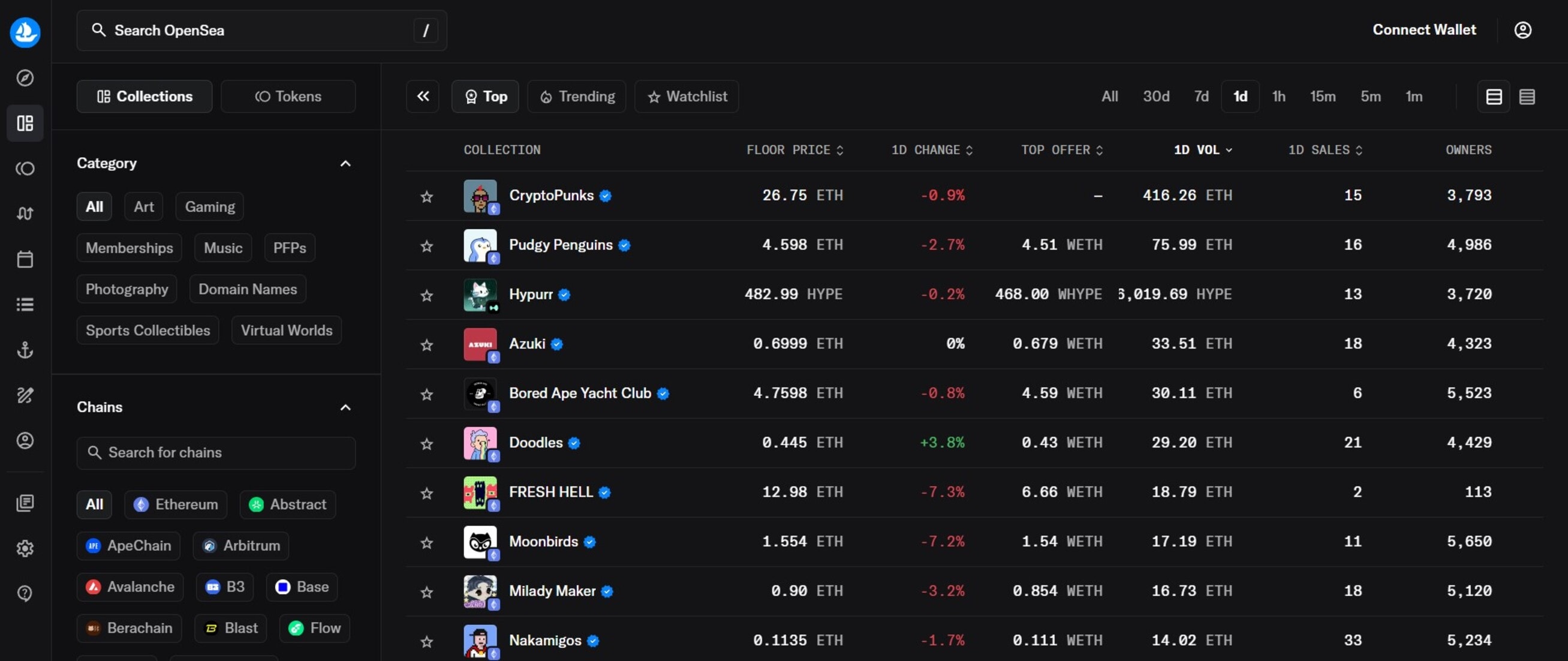

NFT marketplaces are online platforms where NFTs are created, listed, and sold. Choosing the right marketplace determines the audience, minting fees, and blockchain compatibility for an NFT. Some marketplaces are open to all creators, while others focus on curated, high-quality digital painting collections.

Minting an NFT is the process of turning a digital asset into a token on the blockchain. This step makes the asset verifiable, tradable, and officially recognized as an NFT.

Before minting, link a crypto wallet to the chosen NFT marketplace. The wallet stores cryptocurrency for transaction costs and receives payments from NFT sales. Confirm the wallet is compatible with the marketplace and blockchain. Always double-check the website URL to avoid phishing scams. To pick the best crypto wallet for creating, storing, or trading NFTs, check this best crypto wallet for a list of recommended options.

Prepare the digital asset for minting. Ensure the file is high-quality, properly formatted, and finalized, as changes cannot be made after minting. This step may also include adding multiple editions if the collection requires more than one copy of the NFT.

Upload the digital file to the marketplace and complete the NFT listing information. Include:

Once all details are filled in, confirm the minting transaction in the connected wallet. The blockchain technology will record the NFT, linking it permanently to the creator and making ownership verifiable.

After minting, the NFT is ready for sale on the chosen marketplace. NFT creators can select between fixed-price sales, auctions, or timed auctions depending on the strategy. Fixed-price listings allow immediate purchase, while auctions encourage competitive bidding that can increase the final price. Timed auctions close automatically after a set period, creating urgency for collectors and attracting attention to the NFT.

Pricing should reflect the uniqueness, quality, and demand for the asset. Researching similar NFTs in the marketplace helps determine a fair and competitive price. Once the listing is confirmed through the crypto wallet, marketplace fees are applied and the NFT becomes available to buyers. Creators can also earn royalties from future resales, ensuring long-term value as the NFT changes hands in the marketplace.

Before selling, remember it’s important to check the rarity and value of your NFT. This how to check NFTs rarity guide shows how to price your NFT accurately based on scarcity and market trends.

Creating NFTs allows creators to sell digital work directly to collectors without relying on galleries, publishers, or other intermediaries. Each NFT includes a permanent record of ownership on the blockchain, giving creators proof of authorship and control over their work.

NFTs also enable the setting of royalties, so every time the NFT is resold, the original creator earns a percentage of the sale. This provides ongoing revenue that traditional digital content cannot guarantee. NFTs offer access to a global audience, expanding reach beyond local markets.

It enables creators to build a community around their work, connecting with collectors and fans who value originality and uniqueness. NFTs also provide opportunities to experiment with new forms of digital content, from artwork and music to virtual items and collectibles. For creators seeking both recognition and income, NFTs offer a modern, flexible way to share and monetize digital creations.

Launching an NFT collection requires more than minting digital files and listing them for sale. A successful launch depends on planning, storytelling, and audience engagement. The tips below focus on building interest, trust, and long-term value for an NFT collection.

Several NFT collections gained popularity by combining strong visual identity, community engagement, and long-term utility. These collections often serve as reference points for new creators entering the NFT space.

NFTs have changed how ownership and creative value are defined in the online space. Creating an NFT involves choosing the right digital asset, selecting a suitable blockchain, using a secure wallet, and minting the asset on a trusted marketplace. Each step plays an important role in protecting ownership and ensuring visibility.

The cost of creating an NFT depends on the blockchain technology and marketplace used. On blockchains like Ethereum, minting can cost anywhere from a few dollars to over one hundred dollars due to gas fees. Lower cost blockchains such as Polygon, Solana, or Tezos reduce expenses significantly, making NFT creation more affordable for beginners.

NFTs are legal in most countries. However, laws around taxation, intellectual property, and digital assets vary by location. Creating or selling NFTs using copyrighted material without permission is illegal. Understanding local regulations is important before trading or selling NFTs.

Yes, some marketplaces allow free minting, especially on low-fee blockchains like Polygon. While minting may be free, selling the NFT often involves transaction or minting fees. Free minting reduces entry barriers but does not remove all costs.

NFT creation can still be profitable, but success is no longer guaranteed. Profit depends on originality, quality, marketing, and community engagement. Creators who focus on value, storytelling, and long-term utility have better chances of earning income than those relying on hype alone.

The post How to Make NFTs: A Comprehensive Guide in 2025 appeared first on NFT Plazas.

0

0

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.

0

0