JP Morgan Retirement Guide: 2026 Insights

0

0

J.P. Morgan Asset Management recently released the 2026 edition of its JP Morgan Retirement Guide providing timely 2026 retirement insights for advisors and individuals. The report analyzes household data to expose income gaps, spending volatility, and Social Security readiness challenges. In addition, it emphasizes guaranteed income strategies, tax-smart planning, and small consistent savings boosts. These approaches help people navigate longer lifespans and achieve more secure retirement outcomes.

This article will explore key findings on Social Security claiming trade-offs and the benefits of workplace plans for small businesses. It will cover hidden risks in early retirement spending and practical steps for stronger retirement income planning. Readers will see how real household patterns reveal unexpected pitfalls and opportunities. The discussion also highlights simple changes that can make a meaningful difference over time.

Also Read: Ethereum Foundation Treasury Sale: 5,000 ETH to BitMine

JP Morgan Retirement Guide 2026 Exposes New Income Gaps and Security Risks

J.P. Morgan Asset Management released the JP Morgan Retirement Guide 2026. It offers valuable 2026 retirement insights that highlight growing income gaps and serious security risks. The report draws on anonymized household data from recent years to show real challenges in retirement income planning.

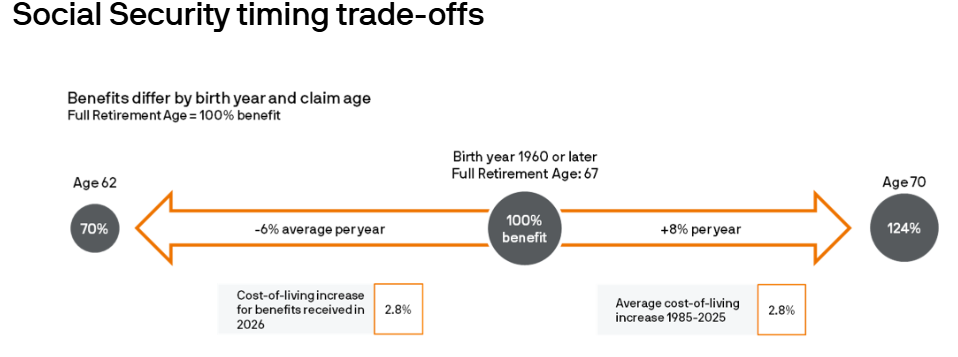

Many workers plan to retire at 65. Yet most actually stop working at 62 because of health problems, layoffs, or unexpected events. When people claim Social Security at age 62, they lock in a permanent cut to only 70 percent of the full benefit. On the other hand, waiting until 70 increases monthly payments by 24 percent above the standard amount. However, widespread myths about the program’s future often lead to poor decisions and lower lifetime income.

The guide also uncovers hidden dangers that threaten retirement stability. Six in ten new retirees see major spending volatility in their first three years, often from surprise medical bills, market drops, or lifestyle shifts. As a result, many households lack enough emergency savings, which leaves them exposed when shocks hit hard.

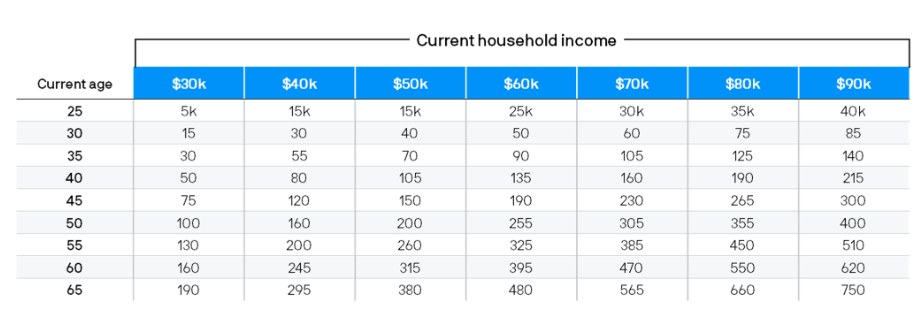

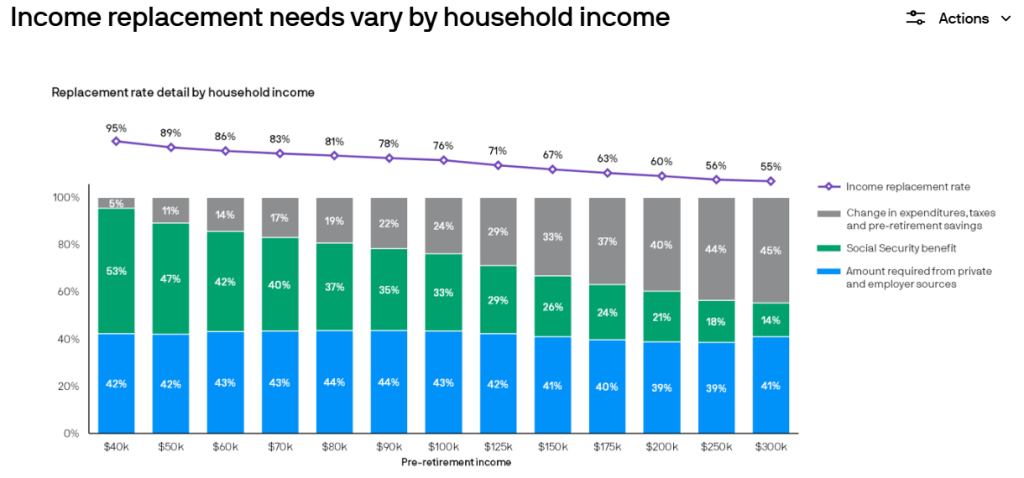

Lower- and middle-income families face the widest income gaps because they need more from private savings after Social Security and reduced taxes. The data shows clear differences in income replacement needs across earnings levels. In fact, households below $90,000 require higher savings rates to keep their standard of living. Without careful steps, these shortfalls grow and weaken long-term security.

Guaranteed income sources provide a strong defense against such uncertainty. Households that rely more on dependable streams, like annuities or pensions, spend with greater confidence. In similar wealth brackets, people with 60/80 percent of assets in guaranteed income spend about 44 percent more each year than those with only 20/40 percent. This gap proves how reliable income helps families handle market swings and health costs without panic.

These findings from the JP Morgan Retirement Guide make one thing clear: Advisors and future retirees must act now on realistic savings targets, smart Social Security timing, solid emergency funds, and more guaranteed income. Taking these steps helps close income gaps, reduce security risks, and build stronger financial protection for the years ahead.

Also Read: Alibaba Earnings: Cloud Growth and AI Expansion in Focus

How the JP Morgan Retirement Guide Shapes 2026 Income and Spending Trends

The JP Morgan Retirement Guide 2026 provides actionable 2026 retirement insights. These directly influence how people approach retirement income planning and daily expenses ahead. Advisors now use its data-driven findings to guide clients toward more predictable income streams and controlled spending patterns.

In particular, small consistent savings increases stand out as a powerful tool. Even a 1 percent boost in savings rates helps build stronger reserves and can cover nearly nine years of Medicare costs over time. As a result, this encourages workers to adopt auto-escalation features in plans. These features gradually raise contributions and improve overall readiness.

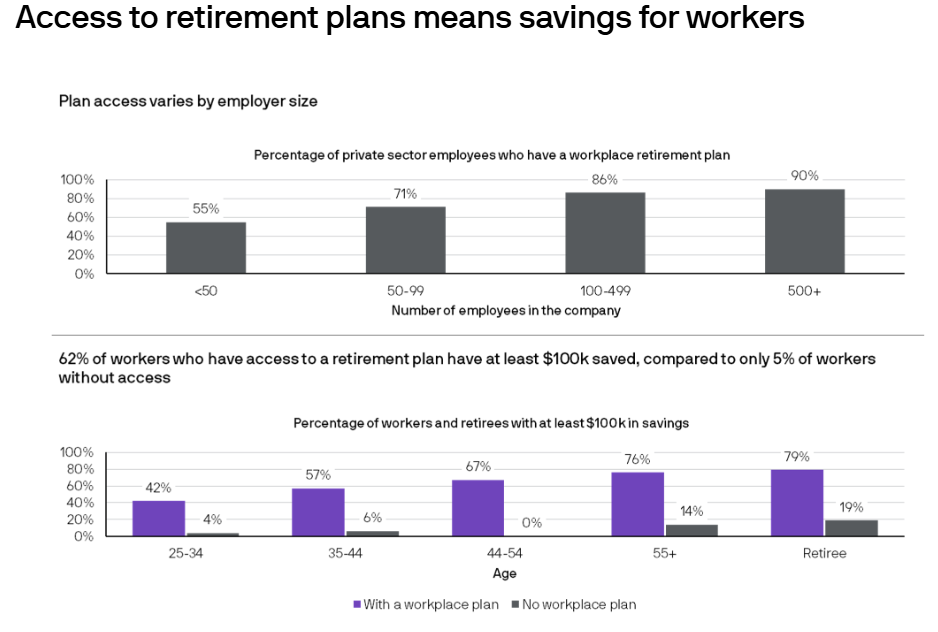

Workplace retirement plans play a bigger role, especially for small businesses. The guide shows that 62 percent of employees with access to such plans save at least $100,000, compared to only 5 percent without one. Small firms now have easier options like SIMPLE IRAs or low-cost 401(k)s, plus auto-enrollment to lift participation.

Additionally, these changes help more people generate reliable income in retirement and reduce reliance on volatile sources. As a result, retirement spending trends shift toward greater stability for middle-income households.

Guaranteed income strategies gain even more attention for shaping confident spending. Households with higher allocations to dependable sources, such as annuities or pensions, spend up to 44 percent more annually in similar wealth brackets. This happens because reliable floors cut fear during market dips or health surprises. In addition, the guide highlights how blending guaranteed income with flexible withdrawals lowers overall volatility and supports sustainable lifestyles well into later years.

Tax-smart approaches also steer future trends. Diversifying between traditional and Roth accounts gives retirees control over taxes and Medicare premiums. Strategic Roth conversions in lower-tax periods can save significantly and preserve more income for spending. Combined with updated 2026 contribution limits and tax brackets, these tactics help families keep more of their savings working longer.

The JP Morgan Retirement Guide pushes a forward-looking view for 2026. It urges proactive steps like building emergency funds, timing Social Security wisely, and prioritizing guaranteed elements. These recommendations help reshape retirement income planning and lead to steadier, more enjoyable retirement spending trends despite longer lifespans and economic shifts.

Also Read: BTC, ETH, SOL News: $71K Bitcoin holds amid Iran risks, Trump meme coin surges

Final Words

The JP Morgan Retirement Guide 2026 paints a clear picture of today’s retirement landscape. It exposes real income gaps and security risks that catch many off guard. These include early Social Security claiming penalties and spending shocks in the first few years, as well as uneven readiness across income levels.

At the same time, the guide offers practical paths forward. Guaranteed income strategies, small but steady savings increases, workplace plan access for small businesses, and tax-smart moves all help build stronger foundations and more predictable outcomes.

These findings urge action now rather than later. Advisors and individuals who embrace realistic targets, reliable income sources, and flexible planning stand a better chance of navigating longer lives with confidence. By addressing vulnerabilities head-on and shaping smarter retirement income and spending trends, the JP Morgan Retirement Guide equips people to achieve greater financial security in 2026 and beyond.

0

0

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.