Gate Ventures Insights: DeFi 2.0 — Curator Strategy Layers Rise as RWA Emerges as a New Foundational Asset

0

0

TL; DR

- Lending is evolving from a “direct-to-protocol model for everyone” toward a structure of “protocol infrastructure + strategy layer.” Curators package institutional-grade risk management, portfolio construction, and routing into non-custodial vaults, with their share steadily increasing. Meanwhile, the growing complexity of RWA is making verifiable risk frameworks such as PoR and DVN increasingly essential.

- RWA are no longer merely held on-chain; they are evolving into yield-bearing, collateralizable, and composable building blocks for on-chain strategies. Platforms and Curators are driving the growth of multi-asset RWA vaults and related derivatives, while institutions are increasingly integrating with DeFi through infrastructure-level partnerships.

- CEXs and wallets focus on user acquisition, user experience, and compliance, while DeFi handles yield execution, settlement, and risk management. In practice, users access “one-click” lending and yield products on CEX platforms, with the underlying strategies driven by on-chain protocols and Curator-managed vaults.

- As the yield layer scales, projects are expanding into payments, accounts, and cards—forming a closed loop from “save → grow → spend.” Whether this model can scale will depend on whether regulation can establish baseline safeguards and clear accountability, while preserving the advantages of on-chain verifiability.

Introduction

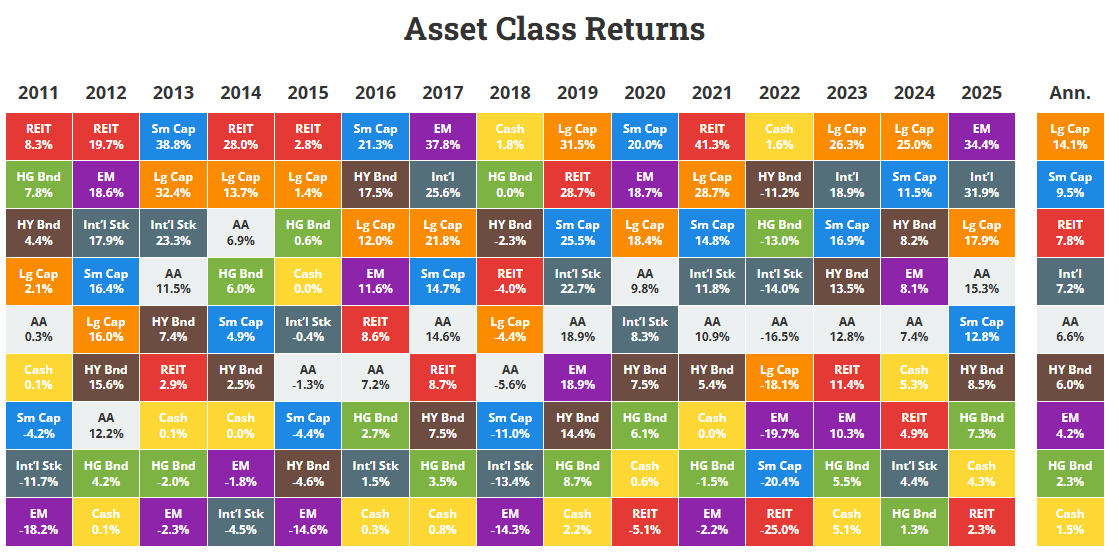

The evolution of DeFi has moved through several distinct phases. From the early days of liquidity mining and simple yield aggregators to the more recent surge in strategies such as looped lending and Pendle points farming, the surface mechanics of yield generation may appear to be constantly changing. Yet the underlying logic has remained remarkably consistent: returns are earned by taking on identifiable forms of risk and receiving compensation for doing so. In this respect, DeFi yield is fundamentally no different from yield-generating assets in traditional finance.

Source: Novelinvestor

Source: Novelinvestor

Take cash and Treasury bills as an example. These assets are among the closest instruments to being “risk-free” in modern financial systems, typically represented by short-term U.S. Treasuries and money market funds. Historical data suggests that their long-term nominal returns average around 3.3%, while real returns—after adjusting for inflation—are close to zero. In essence, investors are compensated almost entirely for the time value of money.

These instruments carry minimal credit risk and very limited duration exposure. The trade-off, however, is clear: inflation steadily erodes purchasing power, making them more suitable as short-term capital parking vehicles rather than long-term wealth accumulation tools.

Bonds, by contrast, reflect the classic logic of earning yield by lending capital and bearing risk. Whether issued by governments or corporations, different levels of credit quality correspond to different return profiles. Historically, investment-grade bonds have delivered nominal returns of roughly 4–4.6%, while high-yield bonds have averaged around 6–8%.

These returns compensate investors for credit risk, duration volatility, and liquidity risk. The trade-offs are equally clear: bond prices can decline sharply during tightening cycles, real returns may turn negative in high-inflation environments, and in cases of default or restructuring, investors may face irreversible losses of principal. (1)

The same logic applies to DeFi.

DeFi has long been associated with the perception of high returns. However, this perception does not stem from the creation of an entirely new wealth-generation model. Rather, it reflects the fact that investors are often bearing substantially higher underlying risks compared to traditional financial assets. These risks can manifest in several ways.

At the protocol level, there is default risk tied to smart contracts or system design. In looped lending strategies, liquidation risk can arise from the high volatility of the underlying assets used as collateral. Meanwhile, in points farming strategies, returns may be highly uncertain due to factors such as unpredictable TGE valuations or shifting airdrop distribution rules.

As the industry continues to evolve, the DeFi market itself is undergoing a structural transformation. More and more projects are actively pursuing sustainable value creation, either by deepening their core products or expanding along the upstream and downstream value chain to strengthen their positioning.

The goal is to build protocols into long-lasting financial infrastructure, rather than relying on the early-stage model of “growth at all costs” driven by heavy subsidies, airdrop incentives, or unsustainably high APYs to attract retail liquidity.

Based on the observations above, we will further explore several key emerging trends in the current DeFi market.

Trend 1: Lending Markets Become Modular, Driven by Risk Curators

Source: Bitwise X

Source: Bitwise X

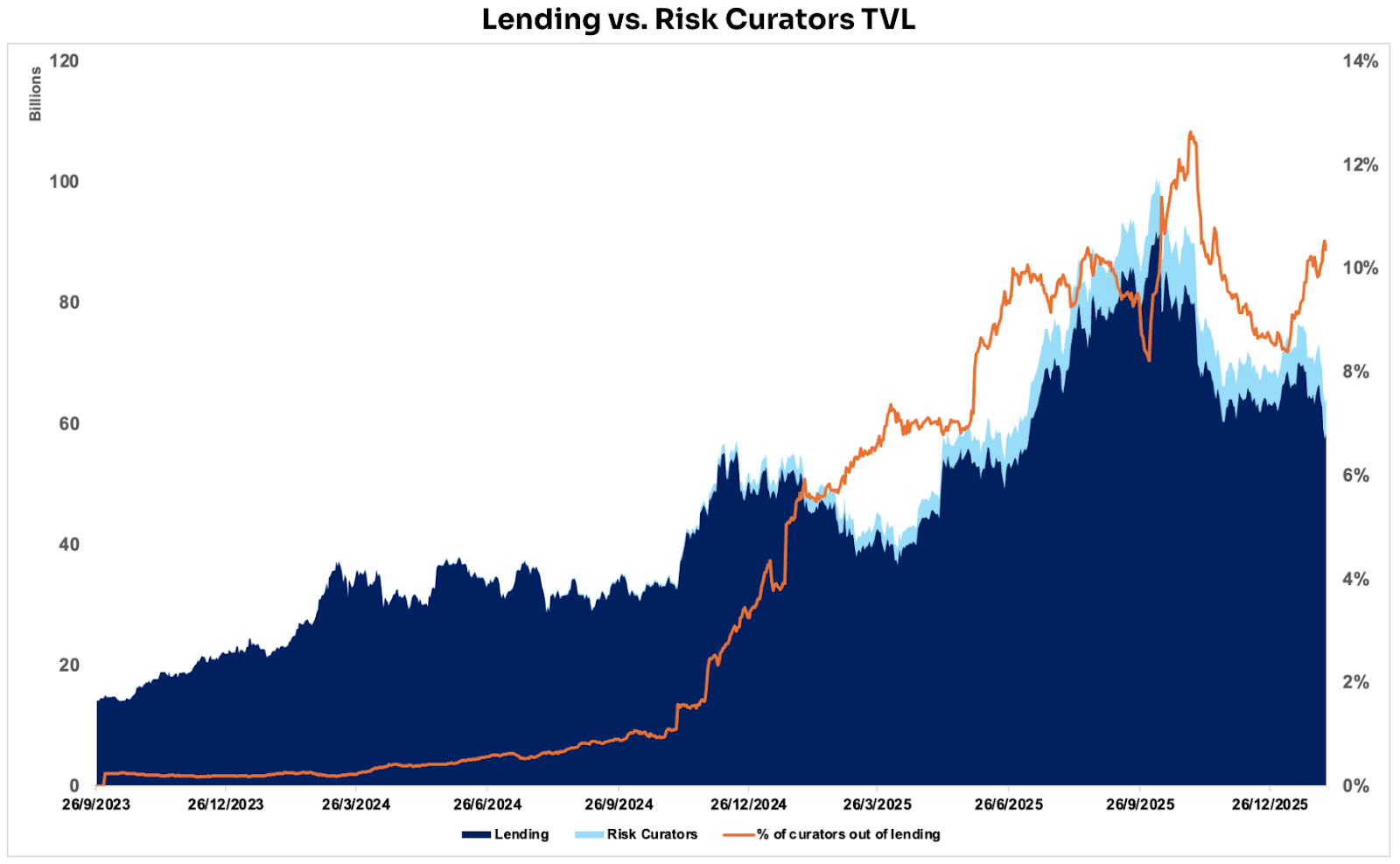

The on-chain lending market has successfully grown into a major DeFi vertical, thanks to its high settlement and execution efficiency as well as powerful composability. The total value locked (TVL) in this space currently stands at roughly $58 billion. Recently, Bitwise announced the launch of a non-custodial vault on Morpho, where it acts as the Curator, deploying dedicated teams for strategy development and risk management.

In the design of DeFi 1.0, all participants were “structurally equal” at the protocol level: the same interest rate models, the same liquidation rules, and the same publicly available information. Users interacted directly with the protocol itself, without any explicit intermediary layer providing professional risk management or strategy execution on their behalf.

Under this structure, more complex and sophisticated strategies—such as cross-market rebalancing, dynamic risk management, interest rate forecasting, and portfolio optimization—were typically executed privately by institutions or professional traders. These strategies were neither productized nor made available to ordinary users in a composable form.

While the protocols themselves were open, the real capabilities for yield optimization and risk management remained concentrated in the hands of a small group of specialized participants.

It is in this context that vault and Curator models began to emerge. Building on the openness of DeFi 1.0, they introduce a verifiable, non-custodial strategy layer that structures the risk management and yield optimization capabilities once limited to a small group of institutions, making them more transparent and accessible to a broader set of on-chain participants.

On protocols like Morpho, Curators allocate user capital across opportunities with different risk–return profiles according to their strategies, dynamically adjusting positions based on ongoing risk assessments and expected returns.

Source: DeFillama

Source: DeFillama

Data show that since the emergence of the Risk Curator, the share of lending protocol TVL managed by curators has steadily increased. It once peaked at nearly 13% and currently hovers around 10%. Within the ecosystem today, Steakhouse Financial, Sentora, and Gauntlet have emerged as the three leading Curators, each managing over $1 billion in on-chain lending positions.

Source: Token Terminal

Source: Token Terminal

How have these on-chain asset managers achieved rapid growth over the past few years?

The key driver is not a question of “who depends on whom,” but rather that as infrastructure matures and specialization deepens, both the supply and demand sides of the market are unlocked simultaneously.

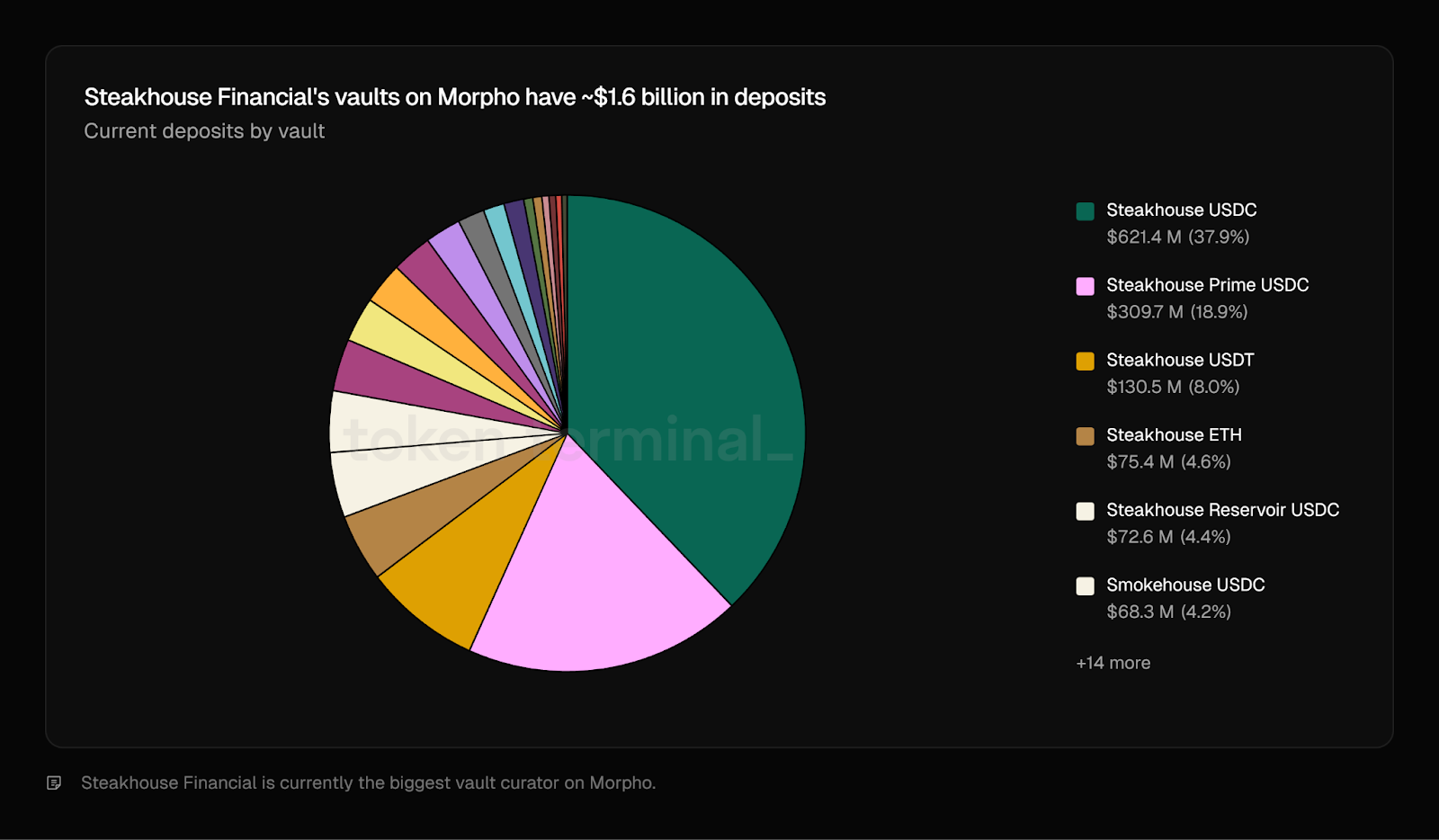

Take Steakhouse Financial as an example: its managed positions on Morpho now account for nearly 20% of the protocol’s total TVL, primarily concentrated in blue-chip assets such as BTC, ETH, and stablecoins, including various synthetic or wrapped forms. This growth resembles a mutually reinforcing loop: Morpho provides the rails and scalable market structure, while Steakhouse packages its strategies, risk management, and product capabilities into non-custodial asset management products that can be widely adopted.

(1) Product Layer: Strategy Layer Packaged as Accessible “Non-Custodial Funds”

- Morpho provides standardized Vault/Market interfaces and execution layers, enabling capital to be routed across multiple markets.

- Steakhouse packages its risk selection and allocation logic into Curator products, allowing users to achieve improved risk-adjusted returns without having to select markets or configure parameters themselves.

(2) Risk Management Layer: Replacing “Trust” with Verifiable Mechanisms

- Steakhouse mitigates tail risks from strategy adjustments through mechanisms such as timelocks, delayed changes, and access controls.

- Meanwhile, the Morpho ecosystem continuously evolves Guardian mechanisms—for example, pausing certain operations during anomalies to prevent obvious errors or malicious parameter changes—further enhancing replicability and stability.

(3) Distribution Layer: Expanding from On-Chain Natives to a Broader User Base

- Coinbase’s USDC Lending on Morpho exemplifies a “channel distribution + DeFi execution + Curator risk management” model: Morpho provides the rails, while Curators deliver yield products that are easier for users to adopt.

- Steakhouse also functions, to some extent, as a distribution channel. When its clients seek on-chain yields, capital naturally flows into Steakhouse-managed vault products on Morpho. This creates a positive feedback loop: Steakhouse scales its assets under management while indirectly driving incremental TVL for Morpho, benefiting both the asset manager and the underlying protocol.

Sentora allocates client funds to Aave Horizon as stablecoin liquidity providers to earn lending spreads, while packaging strategies that provide clients with indirect exposure to various RWAs. Similarly, Gauntlet conducts large-scale capital allocation and vault management on Morpho. (2)

Why is this becoming a trend?

Capital is increasingly concentrating in specialized strategy layers that handle dynamic risk management and portfolio allocation, and are beginning to execute more complex strategies such as RWA-backed lending. Behind these strategies lies a full stack of operational and legal processes, including liquidation mechanisms, custody arrangements, and compliance constraints.

For DeFi to reach broader adoption, someone needs to package what were once complex, institution-grade strategies into accessible products so that everyday users can participate with a single click. Lending protocols could theoretically build and operate this strategy layer themselves, but in practice the development and ongoing maintenance costs often outweigh the economic returns. As a result, many prefer to rely on specialized third-party Curators to take on this role.

This trend is also spreading across other ecosystems; for instance, the largest lending protocol on Solana, Kamino, has begun moving toward a similar modular and vault-based architecture.

Source: Kamino Governance

Source: Kamino Governance

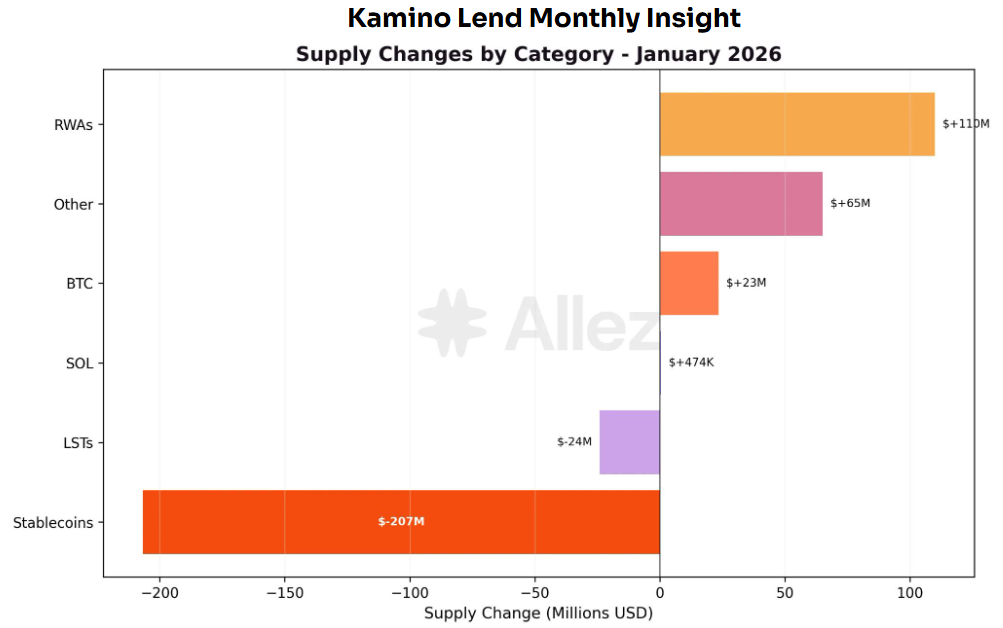

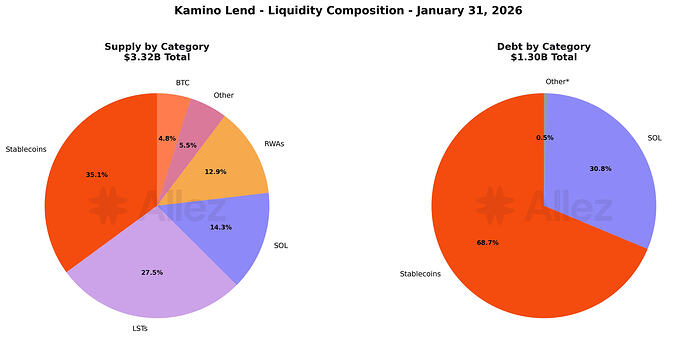

RWA has become Kamino’s fastest-growing category over the past month, with PRIME (+$48M) and syrupUSDC (+$46M) leading the expansion, driven by their attractive yields and leverage-enabled strategies. On the borrowing side, the picture looks somewhat different: stablecoins now account for 69% of all loans, largely supported by the growing number of strategies backed by RWA-based yields (such as PRIME, syrupUSDC, and ONyc). (3)

Source: Kamino Governance

Source: Kamino Governance

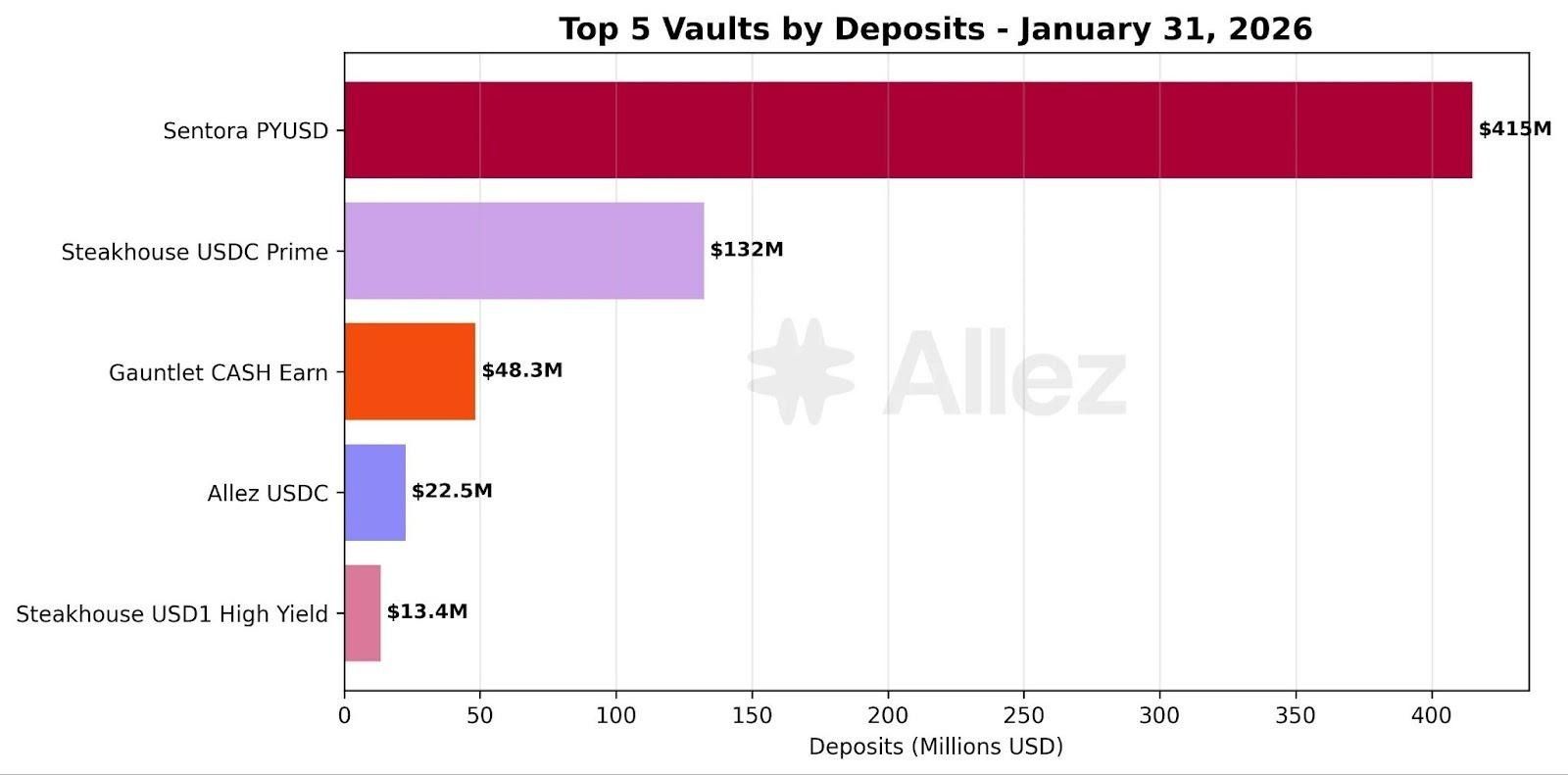

As demand for RWA lending rises, Risk Curators responsible for executing and managing these strategies are simultaneously attracting more deposits and delegated capital. Take Sentora’s PYUSD-related products as an example: last month, they were among the primary beneficiaries of net capital inflows. This lends support to the observation that the complexity of RWA lending is significantly increasing the value and necessity of Risk Curators.

The reason is that RWAs are not merely on-chain collateral. They often involve issuance structures (e.g., SPVs), custody arrangements, liquidation and legal enforceability, compliance constraints (KYC / whitelisting/transfer restrictions), NAV pricing and oracles, as well as maturity and liquidity management.

Consequently, the associated risks are no longer just price volatility and liquidation risk, but a layered combination of credit, legal, operational, and liquidity risks.

Therefore, when DeFi incorporates RWA lending, the role of a Risk Curator evolves from a “yield optimizer” to a “provider of risk screening and structuring capabilities”.

Curators are responsible for screening and layering complex risks, reducing single-exposure risk through portfolio allocation, and productizing institution-grade risk management, enabling broader user participation with lower barriers. If RWA volumes continue to expand, Curators are likely to transition from optional participants to a necessary intermediate risk layer.

Risk Review and Risk Management Framework Reconstruction

The collapse of the “Stream → Elixir → Euler” chain in November 2025 highlighted a key lesson: the greatest risk for Risk Curators does not lie in smart contract security, but in the lack of transparency into underlying strategy and credit risk.

When yields are packaged as simple deposit products, the real risks may already have been shifted and amplified through routing and portfolio construction. Once the strategy layer turns into a black box, a Vault can quickly degrade from an “asset management product” into an “unverifiable risk intermediary.”

Common structural weaknesses can be categorized into four types:

- Centralized control: EOAs and multisigs introduce single points of failure and permission abuse risks.

- Re-staking leverage: Multiple layers of vaults amplify liquidity and liquidation pressures.

- Conflicts of interest: Growth- or scale-driven incentives lead to implicit leverage and tail risk migration.

- Insufficient transparency: Lack of verifiable positions, pricing, backing, and stress scenario disclosures.

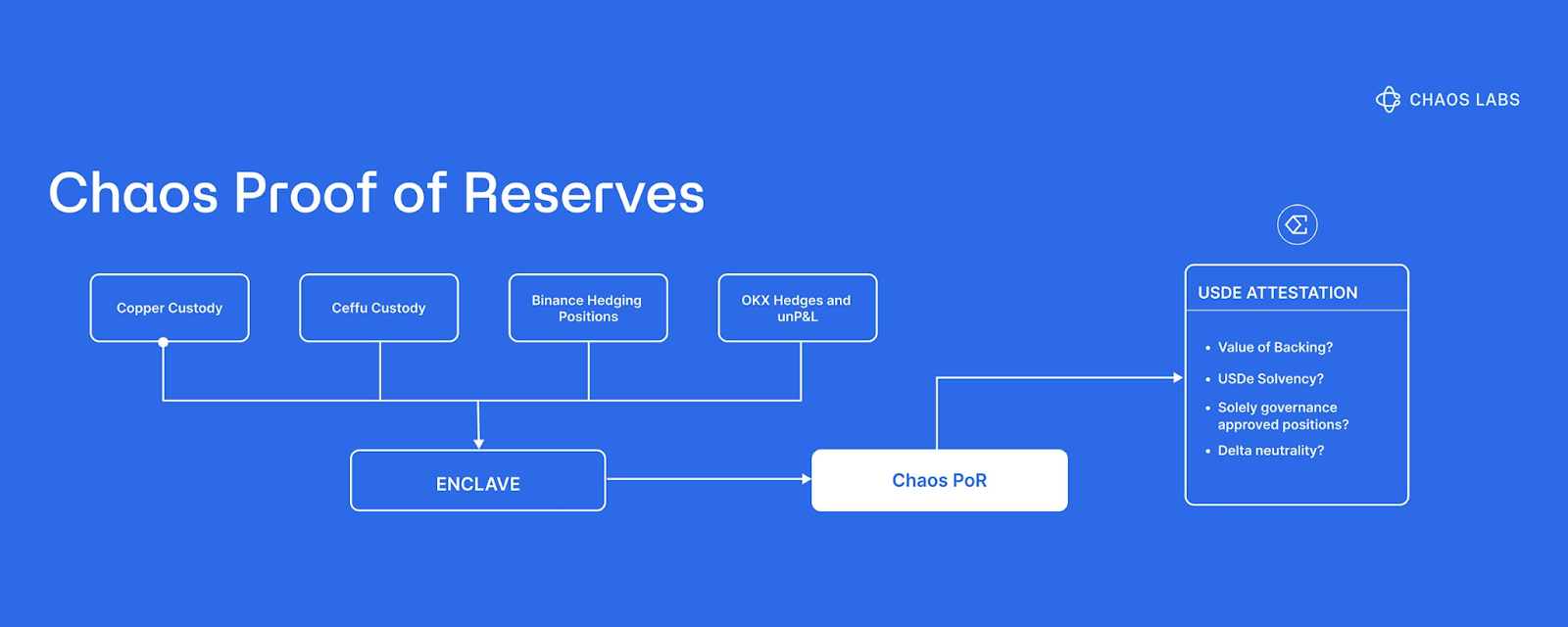

As a result, the market has begun to view PoR (Proof of Reserves) as critical risk-control infrastructure. Taking Chaos Labs’ PoR as an example, its purpose is to address the panic pricing caused by information gaps. After the Bybit incident, Ethena introduced Chaos PoR to improve the visibility and verifiability of USDe reserves, helping reduce cascaded liquidations triggered by speculation during periods of extreme market volatility.

At the mechanism level, Chaos PoR uses automated, multi-layer verification to continuously track three core data streams and output signals that can be consumed by smart contracts: locked reserves, issued supply, and collateralization status.

In essence, it transforms the question of whether reserves are real and sufficient from a matter of narrative or disclosure into a programmable risk input, allowing protocols and users to make decisions based on verifiable evidence rather than market sentiment. (4)

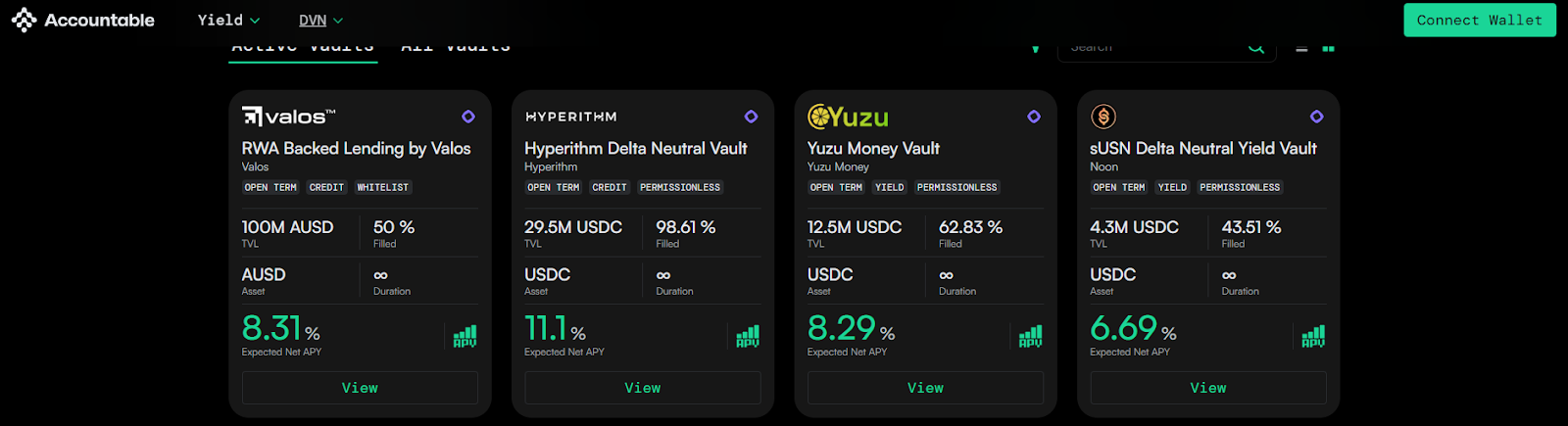

In addition, Accountable offers a complementary solution through its DVN (Data Verification Network), which can be understood as adding a data layer to DeFi vaults and Risk Curators that is both verifiable and privacy-preserving.

Each participant runs a local node, while sensitive information—such as API keys, wallet or exchange accounts, and banking or custody data—remains on their own servers. Data collection and reporting are performed locally and stored in encrypted form.

At the same time, DVN attaches cryptographic proofs to the data and computation results, allowing external parties to verify that the data originates from the specified source, has not been tampered with, and that the aggregation process is trustworthy—without requiring access to individual positions.

Through selective disclosure, Curators only need to publish key portfolio-level metrics (such as assets and liabilities, leverage and collateral coverage, exposure ranges, and liquidity coverage), improving transparency and credibility while keeping detailed strategies confidential. (5)

Compared with PoR, which primarily answers the question of whether reserves are sufficient, DVN goes a step further by bringing the credibility of data sources and the completeness of liabilities into the scope of verifiable assurance. This helps reduce information asymmetry caused by black-box strategies, delayed accounting, and selective disclosure, while significantly improving risk visibility in more complex scenarios such as RWA.

Trend 2: RWA Matures On-Chain as DeFi Use Cases Continue to Expand

Source: Coingeek

Source: Coingeek

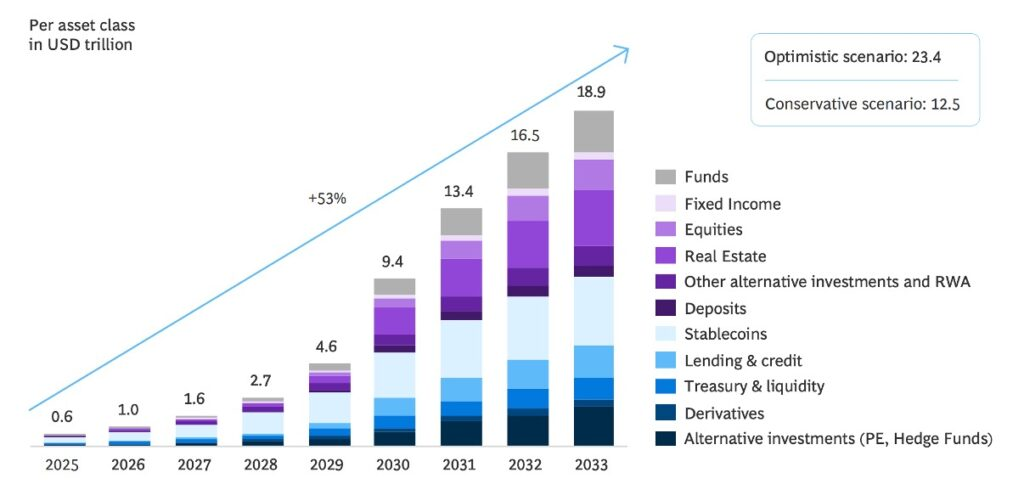

The tokenization of RWA has long become an industry-wide consensus. Multiple forecasts suggest that by 2033 nearly $20 trillion in assets could be tokenized, bringing a wide range of real yield sources—from Treasury bills to reinsurance premiums—into DeFi.

Yet putting assets on-chain is only the first step. In reality, most RWA platforms still operate in a “single-asset, single-position” model, similar to money market funds: users deposit stablecoins, earn a fixed blended yield, and hold the position until redemption, with little active management and limited mechanisms for dynamic rebalancing or portfolio optimization.

(6)For this reason, following the logic of Trend 1 (the rise of Risk Curators), the next category of assets likely to be managed at scale could be multi-asset RWA vaults. In this model, Curators are responsible for screening, underwriting, and continuously monitoring assets, consolidating multiple RWA exposures into an actively managed portfolio. Through a single position, users gain access to more diversified, resilient, and risk-adjusted real yield.

Source: Blockwork @SilvioBusonero

Source: Blockwork @SilvioBusonero

The scale of RWA collateral in lending continues to rise: the current TVL is around $1.6 billion, accounting for roughly 3% of the total lending market, with most activity concentrated on platforms such as Aave, Midas, Morpho, and Kamino. Behind this upward trend is, first and foremost, a shift in the attitude and product strategies of lending platforms:

Lending Platforms

Aave is introducing Horizon, turning RWA lending into a compliant, standalone modular market, effectively bringing RWAs into its core product line. Morpho, meanwhile, leverages Curator Vaults to transform RWA-backed lending into a standardized, distributable product. As for Kamino, the platform has not only launched RWA-related assets such as PRIME, but is also attracting Risk Curators to build and execute a variety of RWA yield strategies on the platform.

Source: Kamino Governance

Source: Kamino Governance

A closer look at Kamino’s collateral supply structure reveals that Stablecoins + RWAs now account for around 48%, surpassing the combined share of SOL + various LSTs (about 42%). It is worth noting that Kamino’s early liquidity and growth were largely driven by looped lending strategies based on native assets and LSTs.

The current structural shift in collateral composition therefore indicates that the platform’s focus is clearly moving toward RWA-backed collateral. This shift also underscores how the strategic positioning and product design of lending platforms themselves are becoming a key force driving the expansion of RWA lending.

Lending Products

Beyond platform-level momentum, product innovation and structural iteration are also bringing new momentum to RWA in DeFi. In the past, most tokenized assets were concentrated in single exposures such as Treasuries or commodities like gold, remaining largely at the stage of simply bringing assets on-chain.

The functional scope on-chain was mainly limited to holding and trading, while development at the application layer remained relatively immature. Take the on-chain gold tokens XAUt and PAXG issued by Tether and Paxos as examples: for a long time they have functioned more like transferable gold certificates, with their utility centered on trading and storage rather than fully developed DeFi applications.

Source: Theo Network Docs

Source: Theo Network Docs

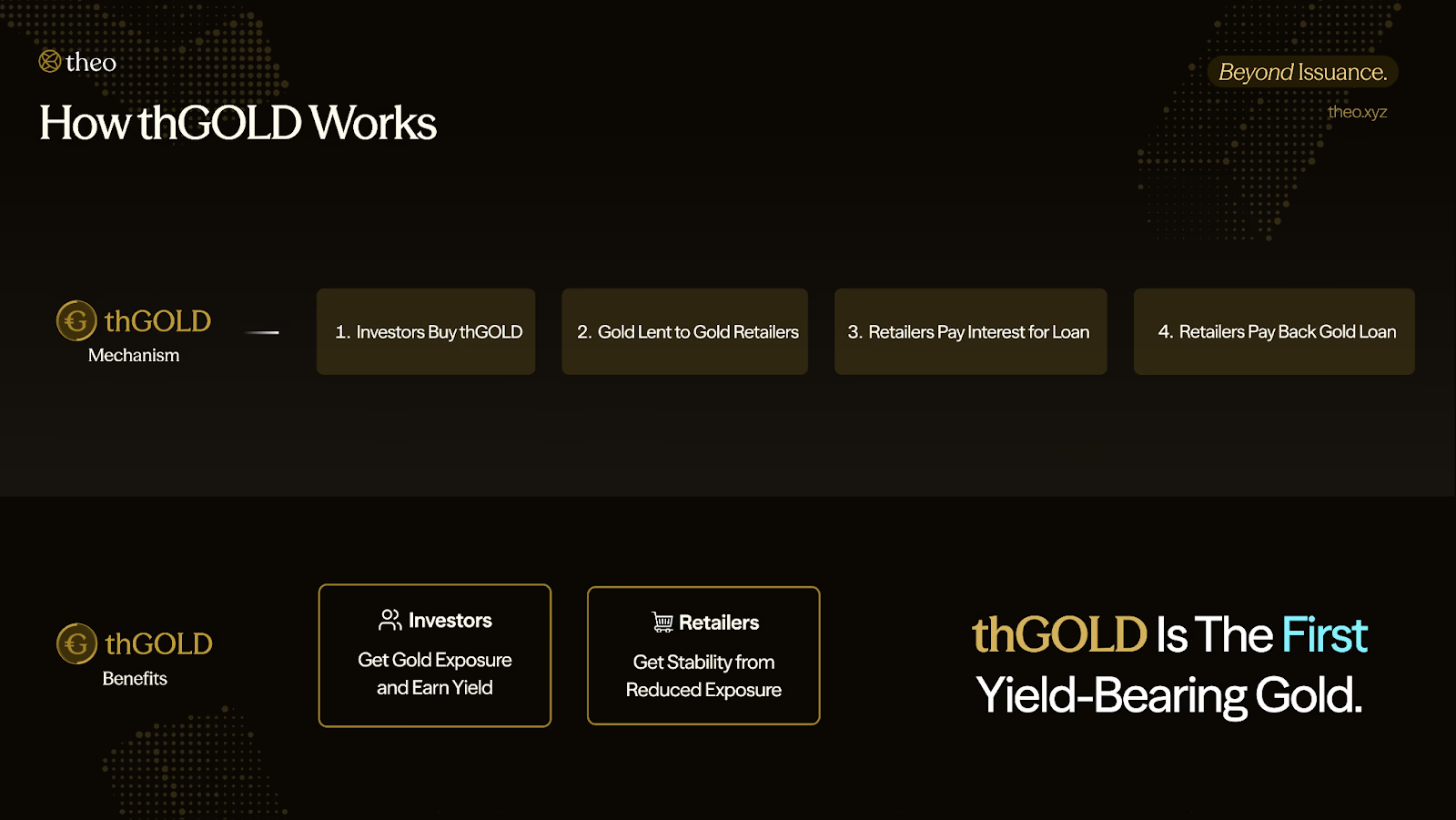

Since 2025, however, the application layer of RWA within DeFi has begun to accelerate noticeably. Builders are transforming RWAs into composable, yield-bearing financial building blocks that can serve as the foundation for strategies. For instance, Theo Network introduced thGOLD, a tokenized yield-bearing gold product.

It generates returns by issuing gold-denominated loans to established gold retailers. Borrowers use the gold for inventory financing and later repay the same quantity of gold plus interest, effectively turning gold into a yield-generating asset with cash flow, currently offering around 2% annual yield. (7)

More importantly, the yield-bearing nature means that on-chain gold is no longer just a static asset. Building on this foundation, thGOLD can also serve as collateral or a strategy component in more complex structured strategies—such as delta-neutral or leveraged strategies—capabilities that traditional non-yielding gold tokens typically cannot provide.

Source: X@rachit

Source: X@rachit

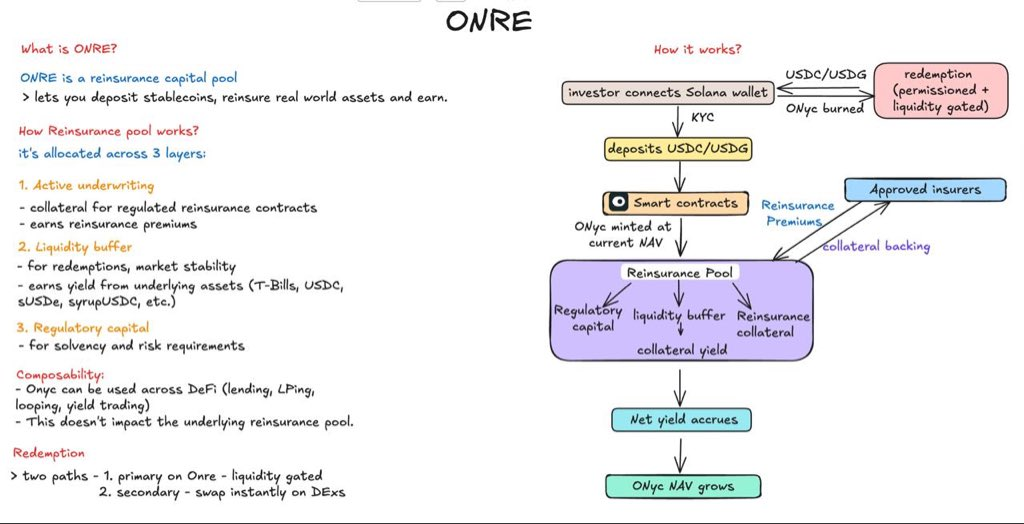

Another example is OnRe Finance on the Solana network. Its yield-bearing token ONyc derives its underlying returns from reinsurance, which can be understood as “insurance for insurance companies.”

Standard insurers underwrite risks such as property or commercial coverage, but when extreme disasters like hurricanes or earthquakes occur, claims can surge within a short period of time. To diversify such tail risks, insurers transfer part of the exposure to reinsurers and pay them premiums; within this structure, OnRe acts as the reinsurance capital provider. (8)

Mechanically, OnRe allocates capital into short-duration reinsurance contracts. Insurance companies typically pay premiums upfront; if no large-scale catastrophe occurs during the coverage period and claim payouts remain below expectations, the premium income minus claim expenses forms underwriting profit, which in turn becomes the yield source for ONyc.

Once this yield structure is brought into DeFi, users can hold and trade ONyc like other yield-bearing assets. Furthermore, ONyc has been integrated into the lending ecosystem of Kamino, allowing users to use it as collateral for looping or leveraged borrowing strategies, effectively combining reinsurance-based real yield with on-chain capital efficiency tools.

Growing Institutional Adoption of DeFi

Traditional financial institutions are entering DeFi in a more infrastructure-oriented way, rather than simply buying tokens or engaging in short-term trading. One key path is integrating compliant RWAs directly into DeFi’s trading and liquidity rails.

A representative example is the Uniswap x BlackRock collaboration: Uniswap Labs partnered with Securitize to connect BlackRock’s tokenized money market fund BUIDL to UniswapX, enabling qualified investors to trade and route liquidity between BUIDL and stablecoins more seamlessly on-chain.

The significance of this collaboration does not lie in the act of issuing assets on-chain itself, but in embedding institutional-grade assets into DeFi’s composable trading layer—opening the door for further use cases such as lending, collateralization, and secondary liquidity. (9)

Another pathway involves institutions committing to longer-term and deeper integrations, effectively betting that on-chain lending will become a mainstream financial market. The partnership between Apollo and Morpho illustrates this direction. Morpho Association reached an agreement with Apollo that allows Apollo, under certain conditions, to acquire up to 90 million MORPHO tokens over a 48-month period.

The strategic logic behind this collaboration is complementary: Apollo contributes institutional capital and credit credibility, while Morpho provides modular lending infrastructure and productized curator/vault capabilities. This combination of “capital + infrastructure” sends a clear signal to the market: on-chain lending is evolving from a DeFi product into a financial rail capable of institutional adoption. (10)

RWA Perpetuals

Tokenized equities have attracted participation from multiple platforms, yet the structural designs vary significantly. Platforms such as xStocks and Backed adopt a custodian-backed 1:1 model, where a custodian holds an equivalent amount of the underlying shares for every token issued. In this structure, investors gain price exposure and 24/7 trading capability, but legally the shareholder of record remains the custodian. Token holders themselves are not directly listed on the company’s shareholder registry.

By contrast, Superstate and Securitize have chosen a different approach. Acting as SEC-recognized Transfer Agents, they directly register token holders in the company’s shareholder registry. Under this model, blockchain is no longer merely an external layer for trading and settlement; it becomes integrated into the shareholder registration and rights verification system itself.

A landmark example occurred in September 2025, when Galaxy Digital completed a tokenized issuance through Superstate’s Opening Bell platform. Holders of the GLXY token were structurally recognized as actual shareholders, entitled to shareholder rights such as voting and dividend distributions. In this framework, the on-chain ownership records are directly linked with the traditional shareholder registry system.

At the same time, market infrastructure is evolving in a similar direction. DTCC, the core clearing, settlement, and custody institution in the U.S. capital markets—responsible for processing securities transactions worth trillions of dollars—has received a “no-action letter” from the SEC. This effectively allows DTCC to begin exploring the tokenization of parts of its securities infrastructure, providing foundational support for bringing securities on-chain in a manner more closely aligned with mainstream market structures. (11)

Current State of RWA Perpetual Contracts

Source: Dune Analytics@yandhii

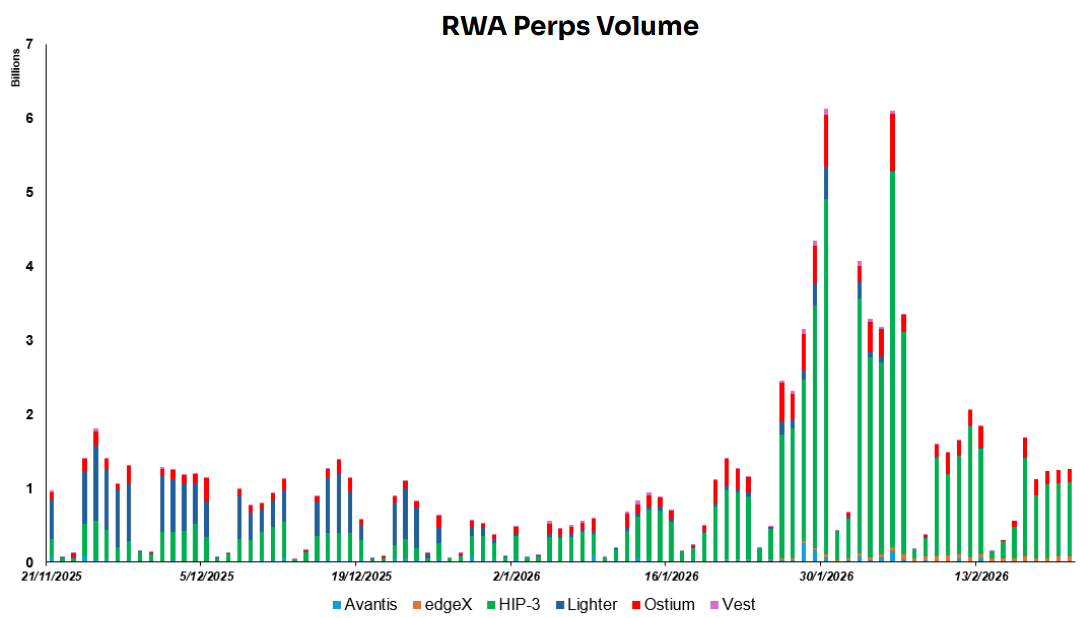

Currently, the daily trading volume of on-chain RWA perpetual contracts is roughly in the $1.5–2.0 billion range, with most activity driven by projects within the Hyperliquid HIP-3 ecosystem, which typically account for more than 60% of total volume. By comparison, the average daily trading volume of U.S. equities is about $51.65 billion, while gold recorded an average daily trading value of approximately $233 billion in 2024. This highlights that on-chain RWA derivatives remain far smaller than traditional markets in terms of liquidity, leaving significant room for future growth. (12)

Source: Lighter X

Source: Lighter X

One of the key advantages of on-chain markets is their ability to open a global liquidity gateway. Assets that were previously constrained by trading hours, geographic access, and brokerage channels can be transformed into standardized contracts tradable 24/7 by a global user base. A clear example is Lighter, which recently launched perpetual contracts for several Korean stocks. This effectively provides non-local investors with a lower-barrier way to gain exposure to overseas equity markets, significantly expanding the accessibility of cross-border stock exposure.

However, stock perpetual contracts do not correspond to any actual share ownership and do not grant holders shareholder rights such as voting rights or dividend distributions. In essence, they are derivative contracts whose pricing is anchored to the underlying stock through indices or oracle mechanisms. The trading process revolves solely around price movements, with settlement occurring based on price changes rather than the delivery or transfer of actual shares.

That said, two major bottlenecks remain prominent in the current market.

First, liquidity fragmentation. Tokenized stocks are distributed across different blockchains and platforms, lacking a unified order book or shared liquidity depth. As a result, trading depth is significantly lower than in traditional markets, prices are more susceptible to market impact, and the ecosystem struggles to support large institutional trades or stable market-making structures.

Second, regulation remains largely “offshore-oriented.” Many related products currently operate in offshore jurisdictions or regulatory environments with relatively lighter oversight. Within the United States, a clear regulatory anchor has yet to emerge. Although many platforms have already launched perpetual-style structured products, the CFTC has not yet established a clear and predictable regulatory framework for perpetual contracts. Regulators are still in the stage of collecting industry feedback and evaluating regulatory boundaries.

The direct implication is that platforms launching perpetual products today are still operating under significant regulatory uncertainty. The legal boundaries surrounding the availability of perpetual contracts to U.S. retail investors remain unsettled. In the long run, a sustainable path will likely depend on the CFTC providing clearer guidance through formal rulemaking or more explicit regulatory interpretations.

Trend 3: DeFi Becomes the Yield and Execution Infrastructure for Centralized Distribution

USD1 has been integrated into Binance Earn as an interest-bearing asset. Coinbase has launched crypto-backed lending powered by Morpho. Kraken’s DeFi yield products are connected to vaults managed by institutions such as Chaos Labs. Meanwhile, tokens related to Ondo Global Markets have been listed on Gate.

Taken together, these developments point to a clearer trend: in order to scale, DeFi is increasingly choosing to embed itself within the distribution systems of centralized exchanges (CEXs) and wallets—such as Earn products, lending services, and wallet mini-apps—rather than competing with them directly at the user entry layer. In this structure, CEXs and wallets handle user acquisition, productization, and user experience, while DeFi protocols handle execution, settlement, risk management, and composability. The result is a division of labor in which distribution happens through centralized channels, while yield generation and execution occur on-chain.

First, CEXs and major wallets possess stronger user acquisition and conversion capabilities. They already have large user bases, low-friction login and trading flows, and mature fiat on-ramps and customer support systems. This allows them to build a smooth product funnel from “buying” to “earning” to “borrowing.” For most users, interacting directly with on-chain protocols often involves higher learning costs and operational friction—such as wallet management, gas fees, cross-chain transactions, and signing approvals. Users must also deal with heightened risk awareness, including smart contract vulnerabilities, phishing, and authorization errors. By contrast, the one-click experience offered by CEXs is closer to traditional financial services, which naturally leads to higher conversion rates.

Second, trust and compliance form a key moat at the entry layer. Many sources of capital—particularly more conservative retail users and institutions—are not short of yield opportunities; rather, they need to feel confident that a product is safe and permissible to use. CEXs are more mature in areas such as brand credibility, risk management processes, KYC and AML compliance, jurisdictional adaptation, risk disclosure, and clearly defined product liability. This reduces users’ psychological barriers related to black-box strategies, scams, or irreversible losses. In other words, CEXs are better positioned to package complex on-chain strategies into financial products that are sellable, understandable, and accountable.

This setup also aligns with the commercial incentives of both sides. CEXs want to expand their financial product offerings and increase user asset retention and ARPU, but they do not necessarily want to assume the full technical complexity and risk exposure of on-chain strategies. DeFi protocols, on the other hand, seek stable capital at scale but lack the most effective distribution channels and the capacity for user education. The most natural outcome, therefore, is a “centralized front-end, on-chain back-end” model: CEXs and wallets manage user relationships, experience, and compliance boundaries, while DeFi protocols handle yield execution, settlement, and composable expansion—ultimately reinforcing a structural division where distribution runs through centralized channels, while yield generation and execution operate on-chain.

Source: DeFillama, Dune Analytics@ryanyyi

Source: DeFillama, Dune Analytics@ryanyyi

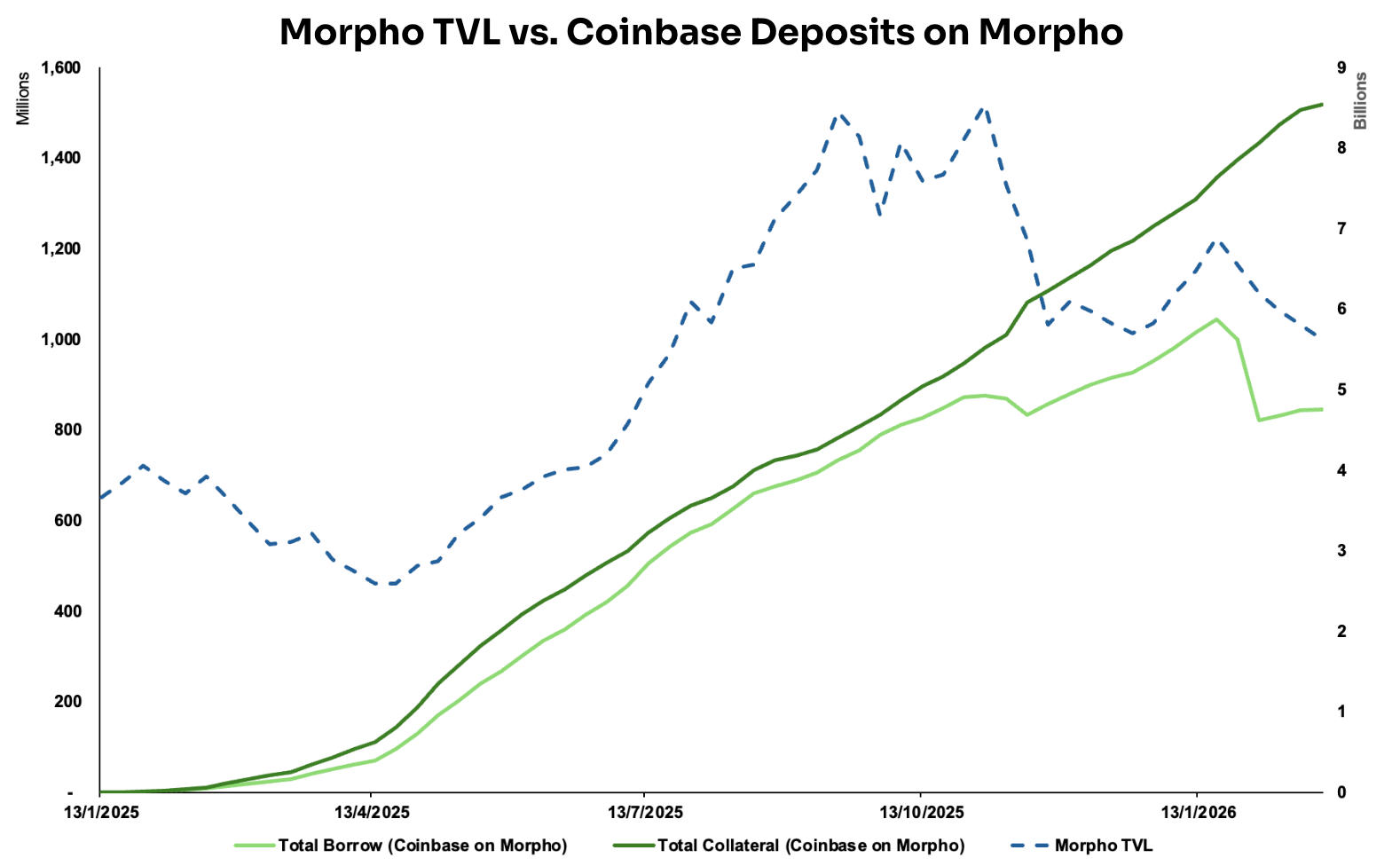

The “CeFi front end, DeFi back end” model is particularly evident in the collaboration between Coinbase and Morpho Labs. Since January 2025, Coinbase has launched a crypto-collateralized lending service that allows users to borrow USD Coin (USDC) using Bitcoin (BTC) as collateral.

In practice, once a user initiates a loan, the BTC is automatically converted into Coinbase Wrapped Bitcoin (cbBTC) and deposited into a Morpho market on the Base blockchain as collateral. The key to this integration is that Coinbase moves almost all of the complexity of on-chain interaction into the backend, allowing users to complete the lending process in a way that feels much closer to traditional financial products. (13)

The infrastructure supporting this experience includes several components: Coinbase Smart Wallet, which automatically binds to the user’s Coinbase account to handle on-chain interactions; Passkeys, used for private key management and transaction signing to lower the barrier to entry; Paymaster, which enables users to pay gas fees with any token; MagicSpend, which allows users to complete transactions even if their on-chain wallet has no assets, by deducting funds directly from their Coinbase account.

The end result is that users only need to hold BTC to “borrow USDC with one click” inside the app, while steps such as wallet creation, bridging, gas management, and transaction signing are handled invisibly in the background.

After the integration went live, the amount of collateral and borrowing flowing into Morpho through the Coinbase channel has shown a steady upward trend. For Morpho, the benefits go beyond the increase in total value locked (TVL).

Partnering with Coinbase provides strong distribution credibility and trust spillover: as an infrastructure layer selected by a mainstream platform, Morpho’s perceived reliability and usability are strengthened. This, in turn, makes it easier to attract additional depositors, curators, and application-level integrations, reinforcing a positive growth loop.

Source: Dune Analytics@ondo_team, @xstocks

Source: Dune Analytics@ondo_team, @xstocks

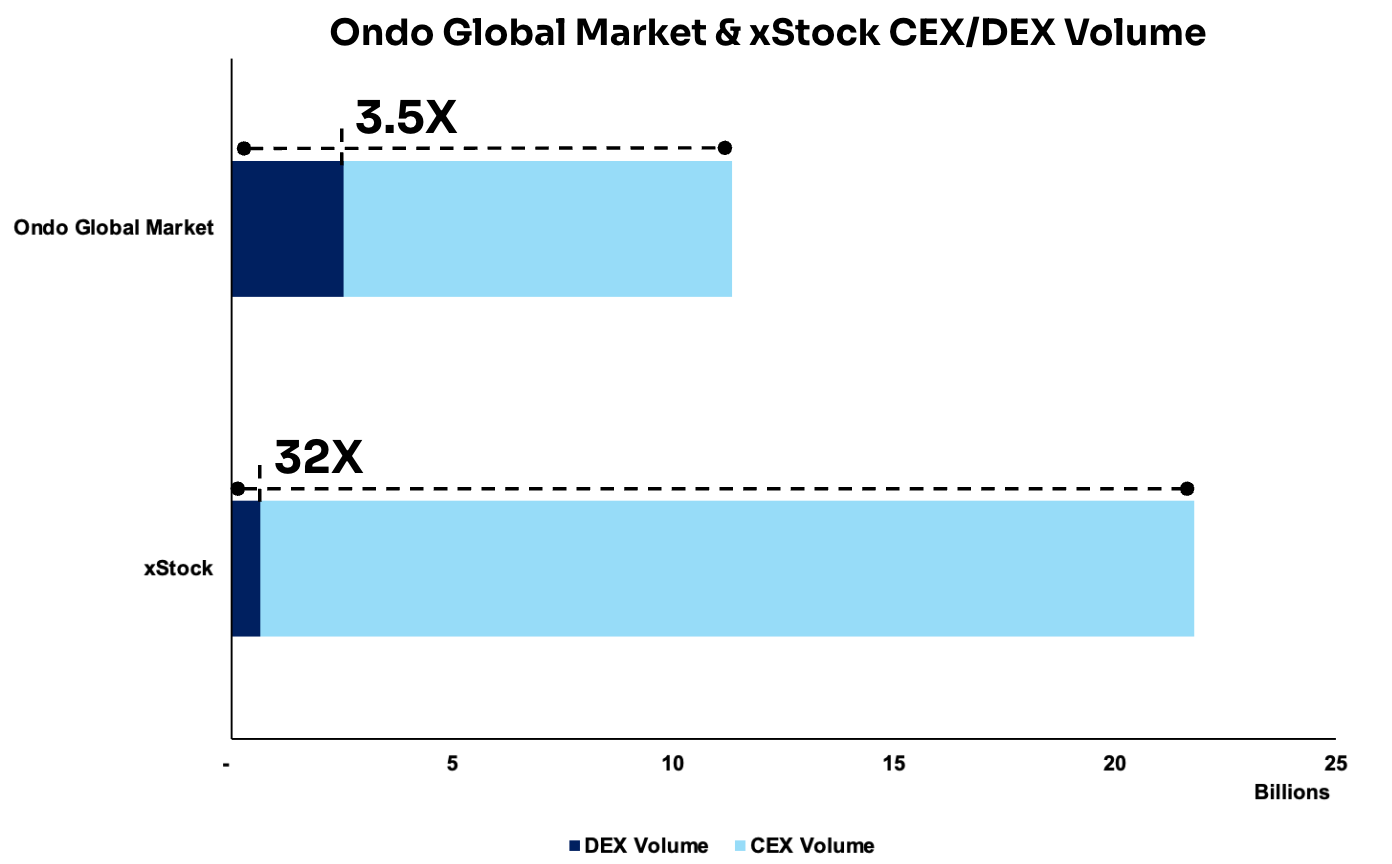

Another representative example is the listing of tokens related to Ondo Global Markets and xStocks on multiple centralized exchanges. Data shows that their trading volumes on CEXs significantly exceed those on decentralized exchanges (DEXs), reaching approximately 3.5× and 32× the DEX volumes, respectively.

This gap highlights a practical reality: at the current stage, CEXs remain the most concentrated liquidity hubs and the most efficient matching venues. They naturally aggregate a larger user base, enabling deeper order books and faster price discovery during the early stages of asset listings—thereby significantly enhancing overall market liquidity.

Trend 4: DeFi Vaults Upgrading into On-Chain Neo-Banks Integrating Payments, Savings, and Yield

At the macro policy level, the regulatory pathway for banks and institutions to participate in digital assets is becoming significantly clearer as stablecoin legislation takes shape. U.S. regulators such as the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and the Federal Reserve have gradually begun rolling back earlier restrictive guidance, while signaling more practical regulatory space in areas such as custody, settlement, staking, and stablecoin issuance.

At the same time, regulatory frameworks such as the EU’s Markets in Crypto-Assets Regulation (MiCA), along with emerging policies in jurisdictions including Japan, Hong Kong, and the United Kingdom, generally emphasize reserve adequacy, transparency, and risk management.

Taken together, the external environment is increasingly providing builders with clearer compliance anchors, while also laying the institutional groundwork for products like Neo Finance that bridge regulated financial systems and on-chain infrastructure.

On the infrastructure side, the cost of modern L1 and L2 networks has fallen significantly, while account abstraction has matured to the point where on-chain financial products can deliver experiences approaching the smoothness of Web2. For example, users can create a smart wallet simply by registering with an email address. After linking a bank account, they can deploy funds into DeFi vaults—such as those on Morpho Labs—to earn yield, and then spend that yield directly through a debit card.

More importantly, the core capabilities required to build a neobank have become highly modular and close to “plug-and-play.” Key components such as payment accounts, fiat on/off-ramps, card issuance, KYC, and wallet custody have been broken into standardized modules by infrastructure providers.

For example: Teams needing virtual USD accounts and payment settlement rails can integrate solutions from Bridge; those aiming to quickly launch crypto-linked payment cards can use infrastructure from Rain; low-friction onboarding and wallet/identity integration can be handled through Privy. As a result, teams can assemble these modules as needed to build products quickly, without relying on deep banking partnerships or building complex compliance capabilities from scratch.

These structural shifts are directly shaping the strategic direction of many DeFi projects. In order to reach a broader user base, an increasing number of teams are evolving toward integrated banking-like services. For example, ether.fi has expanded from a liquid staking platform into a one-stop DeFi bank, productizing savings, yield generation, and payments.

Aave has also extended beyond its original lending protocol to develop mobile applications that provide banking-like deposit, withdrawal, and fund management experiences.

Meanwhile, AllScale is building a stablecoin-based account infrastructure aimed at global micro-enterprises, enabling cross-border payments and financial operations for a new generation of “global individuals and small teams” through a self-custodial banking model.

Similarly, Tether, through its investment in Plasma blockchain, is extending stablecoins beyond the issuance layer toward a broader settlement network and application layer, with the goal of incubating payment, clearing, and account-based financial infrastructure within its own ecosystem.

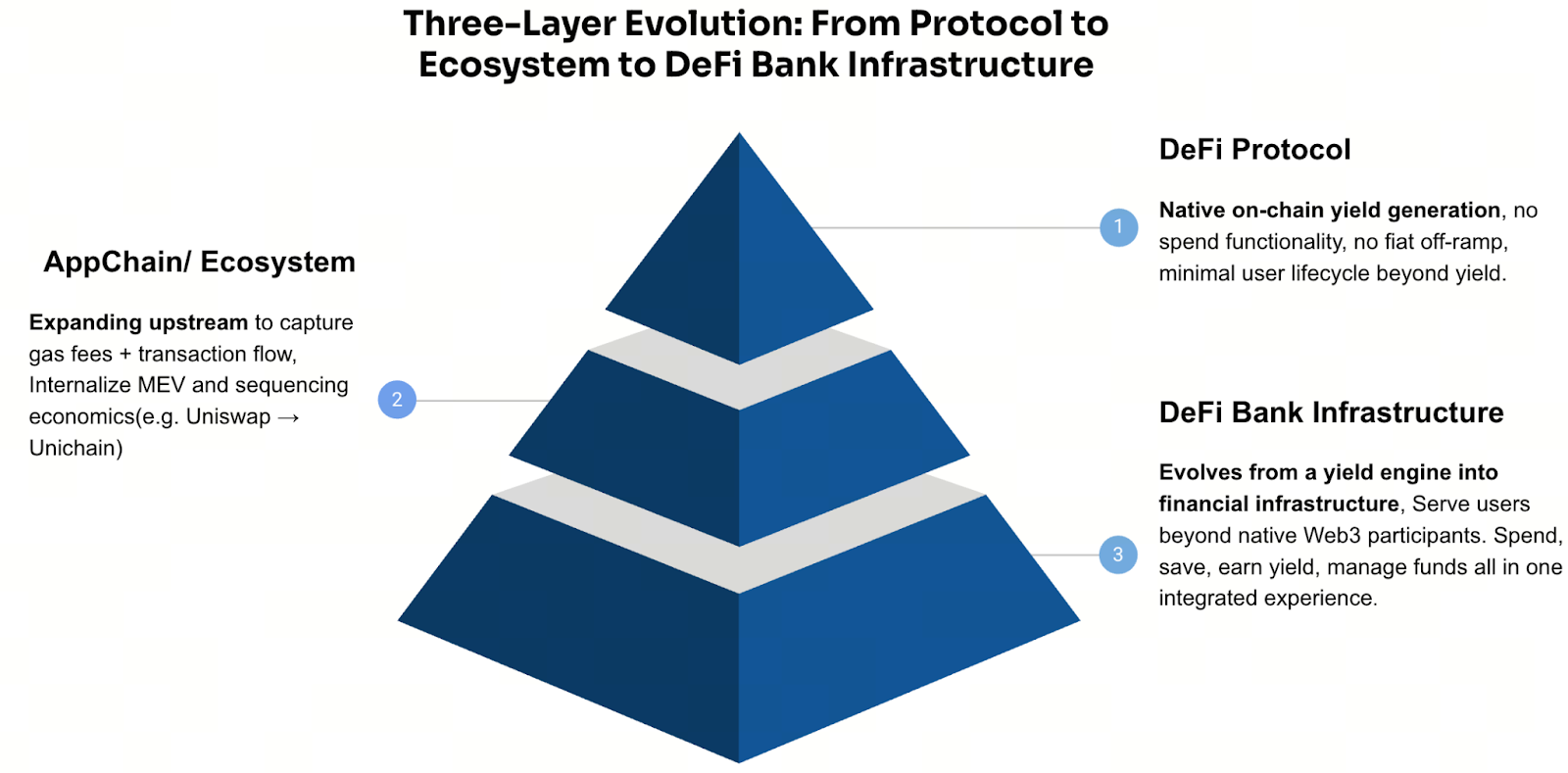

Of course, this shift also represents a downstream expansion driven by scale. As yield layers such as vaults and lending protocols grow larger, projects naturally evolve from single-purpose protocols toward a more complete financial stack. The common trajectory tends to follow a path of “protocol → ecosystem/chain → financial applications.”

The logic behind this shift is also pragmatic and, to some extent, valuation-driven. Relying solely on yield distribution tends to impose relatively limited ceilings on both monetization and valuation multiples. However, once capabilities expand into areas such as payments, custody, account infrastructure, and user relationship management, projects can build more durable, compounding revenue structures and unlock significantly higher valuation potential.

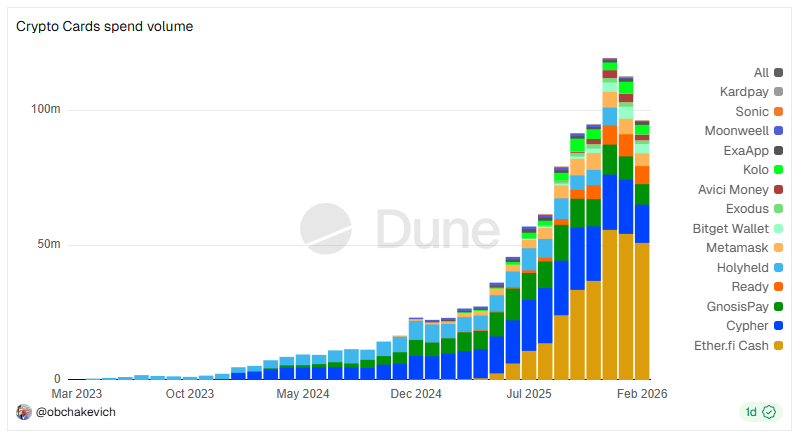

Source: Dune Analytics @obchakevich

Source: Dune Analytics @obchakevich

A good example is ether.fi. The project initially positioned itself as a liquid staking token (LST) protocol, converting Ethereum into tradable yield-bearing assets—eETH and weETH—allowing users to maintain liquidity while continuing to earn staking rewards.

Through deeper integrations with DeFi platforms such as Balancer and Pendle, the role of eETH/weETH evolved from simple yield certificates into a foundational asset layer that is collateralizable, composable, and strategy-manageable. These assets can be used as collateral for borrowing, leveraged in DeFi strategies, or deployed into vaults for more complex yield structures.

Eventually, ether.fi launched Cash (Account + Card), extending the capability of “earning yield” into everyday spending, forming a typical DeFi banking loop:

- Asset side (LST/vaults): Accumulates TVL and user assets while providing yield generation and strategy management—responsible for the “save” and “grow” functions.

- Liability / payment side (Cash + Card): Provides collateralized spending and payment capabilities.

When users can borrow against their assets to spend, they no longer need to sell holdings to cover daily expenses. This leads to higher capital efficiency and stronger asset retention within the ecosystem. For users, the experience becomes a complete capital lifecycle: Save (Stake / Liquid staking) → Grow (Strategies/Vaults) → Spend (Cash Card) → Repay (Flexible repayment).

More importantly, the early-stage LST protocol provided ether.fi with two critical foundations: user asset deposits and a yield-generation infrastructure. Expanding payment and spending services on top of these layers effectively captures the full lifecycle of user finances—from earning to spending.

This strategy has allowed ether.fi to maintain a leading position in the crypto payment card sector, reaching average monthly spending volumes exceeding $50 million, and illustrating a typical evolution path from yield protocol → asset base → payment accounts and cards → full-stack DeFi bank.

Looking at ether.fi’s DeFi bank evolution, we can observe a relatively standardized layered architecture.

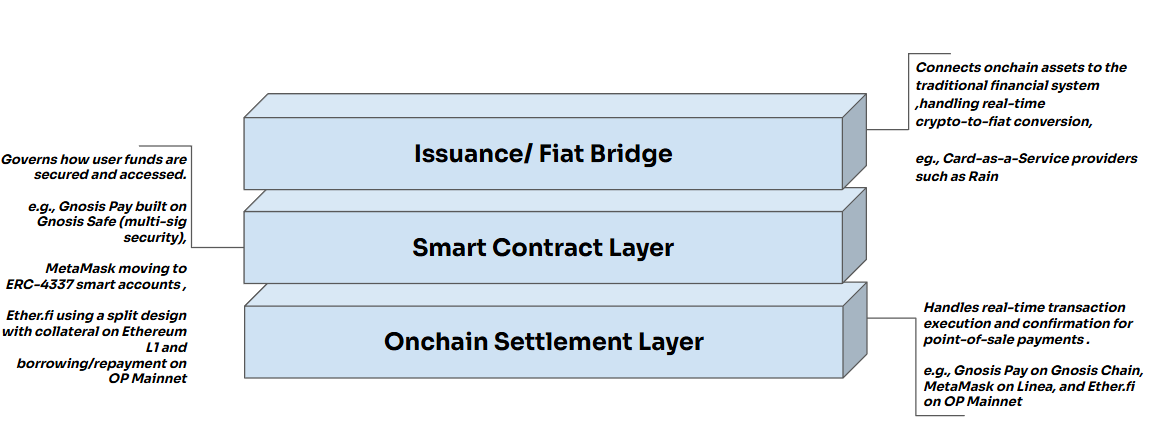

At its core lies a Point-of-Sale Conversion Bridge (POS real-time conversion mechanism). When a user swipes a card at a POS terminal, the system converts the underlying crypto assets into fiat in real time in the backend. Merchants still receive standard fiat settlement, while the final clearing process is handled through traditional payment networks such as Visa or Mastercard.

The entire conversion process remains completely transparent to merchants, making crypto-based spending effectively invisible at the payment terminal while seamlessly integrating with existing financial infrastructure.

Under this mechanism, the full process can be broken down into a three-layer architecture:

Settlement layer: Responsible for fast, low-cost on-chain confirmations on L2 networks for POS payment scenarios. Smart contract layer: Handles secure fund management and execution logic, including multi-signature architectures, the ERC-4337 account system, and collateralized lending mechanisms.

Card issuance layer: Implemented through a CaaS (Card-as-a-Service) platform, enabling real-time conversion from crypto assets to fiat while connecting to banking infrastructure and payment networks such as Visa and Mastercard, thereby enabling seamless acceptance by merchants worldwide. (15)

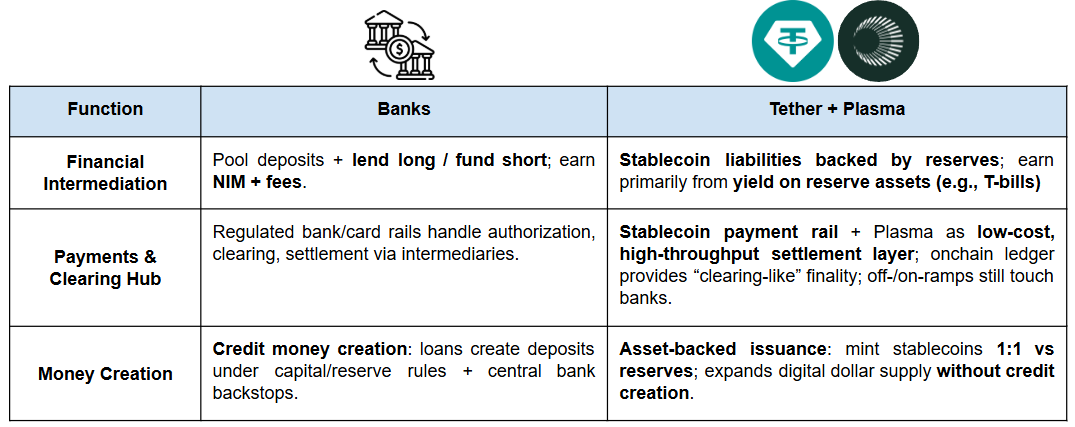

On another front, Tether is also actively expanding downstream into application layers, with its overall positioning gradually moving closer to that of a bank. In general, banks typically perform three core functions:

- Financial intermediation (deposit taking and lending): Banks pool funds from savers and lend them to individuals or businesses with financing needs, generating revenue through interest spreads and related service fees.

- Payment and clearing hub: Banks sit at the center of domestic and cross-border payment networks, handling transfers, clearing, and settlement, as well as processing payment instruments such as credit and debit cards.

- Money creation and policy transmission: Within the constraints of capital and reserve requirements, banks expand deposit supply through lending (effectively creating new money) and serve as key channels through which central bank monetary policy reaches the real economy.

Tether’s strategic investment in Plasma blockchain further strengthens its capabilities along this “digital banking” trajectory:

At the monetary layer, stablecoins provide a widely circulating form of “digital dollars” through issuance. At the payment layer, dedicated stablecoin chains such as Plasma upgrade stablecoins into higher-frequency, lower-cost, and scalable rails for payments and settlement. At the account and asset layer, Plasma enables stablecoins to be embedded into experiences closer to bank accounts—covering storage, management, and yield distribution—thereby strengthening user retention and capital deposits while providing users with a sustainable pathway to earn yield.

Outlook

Whether DeFi banks can scale will depend largely on the fundamental differences between DeFi and traditional banking in their mechanisms of trust. The banking system has evolved over more than four thousand years and is essentially a license-based economy.

Through a comprehensive institutional framework, regulators outsource “trust” to the banking system itself—via clearly defined entry barriers, regulatory licensing, legal accountability, and ongoing supervisory oversight. When users deposit money in a bank, the confidence they rely on does not stem from the moral integrity of any single institution, but from the institutional credibility embedded in the system.

By contrast, trust in DeFi banks is derived more from verifiable system design. Code can be audited, on-chain data is transparent, and collateralization and liquidation rules are executed automatically. The aim is to shift trust away from people and institutions toward rules and execution.

However, the most significant difference lies in the absence of systemic backstops that exist in traditional finance. DeFi systems generally lack protections such as deposit insurance, and they do not have a central bank acting as a lender of last resort (LOLR) during systemic bank runs or liquidity crises. When extreme risks occur, DeFi protocols typically rely on pre-programmed liquidation mechanisms, insurance funds, or risk reserves to absorb shocks.

As a result, whether DeFi banks can achieve mass adoption will ultimately depend on regulation. Only if regulatory frameworks can provide users with comparable baseline protections and clearly defined liability boundaries—without undermining the advantages of verifiability—will large-scale adoption become truly possible.

Reference:

0

0

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.

0

0