How to Use Cashback, Rewards, and HYSA Without Overcomplicating Money

0

0

Cashback, points, and high-yield savings accounts (HYSAs) can add real money to your bottom line—but many people turn it into a spreadsheet hobby. You don’t need that. A simple, rules-based setup captures most of the value with almost none of the hassle.

This guide shows how to pair one or two rewards cards with a single HYSA, automate the flows, and avoid traps that wipe out gains. You’ll see where the easy wins are, what to ignore, and how to keep your system running in minutes per month.

| Aspect | What to Know |

|---|---|

| Core goal | Earn simple, safe yield on cash and steady cashback on spending—without managing dozens of cards or accounts. |

| Cards to carry | One flat-rate cashback card (1.5%–2% typical) for everything; optionally one category card you actually use (e.g., groceries). |

| Payoff rule | Autopay the statement balance in full every month; if you ever carry a balance, stop optimizing rewards and focus on payoff. |

| Savings home | One HYSA at an FDIC/NCUA-insured institution; expect variable APYs. Mid-2026 leaders pay 4%+ APY; rates change. |

| Redeeming rewards | Prefer cash or statement credits. Sweep cash redemptions into HYSA to compound. |

| Maintenance cadence | Quarterly: check your HYSA APY, card annual fees/benefits, and category caps. Make small adjustments, not an overhaul. |

| Risk controls | Disable “minimum only” autopay settings, watch utilization (keep it modest), and avoid offers that require hoops for “up to” rates. |

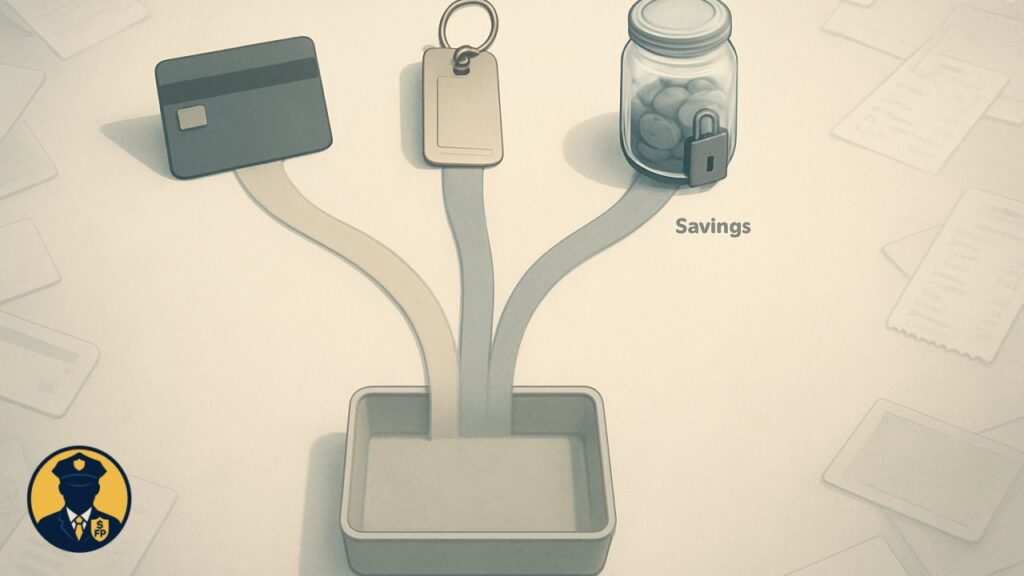

Core Mechanics: How Cashback, Rewards, and HYSAs Work Together

Editor’s note: In 2026, I see readers earning less from the stock-like hacks and more from cleaning up their cash flow. With savings averages still far below top HYSAs and card APRs staying punishing, the winners are the households that automate: one flat-rate card paid in full, one HYSA linked to checking, and a quarterly check-in. Rate caps and shifting promos make headline APYs noisy, so I prioritize stable, insured accounts over chasing tiny bumps. The best optimization is avoiding interest and getting cash working immediately.

Here’s the 80/20 of the system:

- Use a flat-rate cashback card for nearly all purchases. This avoids mental math and category juggling. If you reliably spend in a high-earning category (like groceries or transit), add one category card—but only if the extra steps won’t cause mistakes.

- Always pay the statement balance in full. Interest typically dwarfs rewards. In Bankrate’s latest survey, 47% of cardholders carry a month-to-month balance, and 61% of those have done so for at least a year—evidence that many people erase any reward gains with interest costs (Bankrate).

- Park your emergency and short-term savings in a HYSA. The FDIC’s May 2026 national average savings APY was just 0.38%, while HYSAs commonly pay multiple percentage points more (FDIC). That gap is meaningful on cash you plan to keep liquid.

- Expect variability in HYSA yields. The same FDIC bulletin lists a national rate cap of 4.39% for savings, which helps explain why many advertised HYSA rates cluster in the low-to-mid single digits and why outlier promos may be narrow or conditional (FDIC).

- Shop rates—but only sometimes. June 2026 leaderboards show multiple 4%+ APYs; for example, Varo’s promotional savings advertises 5.00% APY on up to $5,000 with requirements (rate snapshots last updated early June 2026) (Bankrate). Good to know, but it’s rarely worth switching banks for a marginal bump that adds friction.

- Cashback is usually non-taxable. Typical credit-card cashback and purchase-linked points are generally treated like rebates, not income, for consumers. An IRS Chief Counsel memo outlines this accounting view for issuers and notes timing specifics; edge cases (referral bonuses, unconditional payouts) can differ (IRS).

Step-by-Step Playbook

- Map your money flow. List where paychecks land, which bills hit which accounts, and your top spending categories. The goal is to route purchases through one primary rewards card and keep liquid savings in one HYSA you can reach within 1–3 business days.

- Choose your “daily driver” card. Pick one no-annual-fee flat-rate cashback card for everything. Accept that simple 1.5%–2% cash back on all purchases beats complex setups you won’t maintain. If you truly spend heavily in a single category (e.g., groceries), add one category card you can remember to use at that merchant type.

- Set autopay to “statement balance”. In your card app, select autopay for the full statement balance by the due date. If cash flow is tight, keep a small checking buffer and enable alerts for statement posting, payment confirmation, and unexpected large charges.

- Open one HYSA and link it. Choose an FDIC- or NCUA-insured institution with a competitive APY and easy ACH links to your checking. Confirm transfer speeds, any withdrawal limits, and whether you need a linked checking account to earn the top rate. Remember: national average savings APY was 0.38% in May 2026, while many HYSAs pay 4%+—so the move can be meaningful (FDIC; Bankrate).

- Automate your sweep. After payday, transfer a set amount or any checking balance above a threshold into your HYSA. For example:

Keep $1,500 in checking; sweep the excess each Friday.

Small, regular transfers reduce the urge to time markets or chase pennies. - Redeem rewards monthly into cash. If your issuer allows bank transfers, push cashback straight to your HYSA. Otherwise, take a statement credit, then manually move the same amount from checking to HYSA. Avoid sitting on points—programs can devalue and you earn nothing while you wait.

- Do a 15-minute quarterly tune-up. Check: (a) your HYSA APY versus top offers; (b) card annual fees versus actual benefits; (c) whether category caps still fit your spending; (d) that autopay remains set to full balance. Switch only if the net benefit outweighs the switching cost.

Trade-offs: Simple Flat-Rate vs. Chasing Every Perk

There’s a spectrum between “one card, one HYSA” and a binder full of rotating categories and airline partners. The more you chase, the more you must track—and the higher the chance of breakage (missed categories, expired points, interest due to a missed payment).

- Flat-rate wins for most households. Predictable cash beats the mental overhead of juggling multiple programs. If you spend $2,000/month, the difference between 1.5% and 2% is $10/month—nice, but not worth six apps and weekly category checks for many people.

- Category cards are fine if they’re automatic for you. If your grocery card lives in your pantry bag and you never forget to use it at the store, the extra percentage might be worth it. Add only one such card at a time and ensure the cap fits your real spend.

- Travel points can be valuable—but cost time. Portals, transfer partners, and devaluations add complexity. Unless you enjoy that hobby, consistent cash you can move to HYSA is easier and more flexible.

- Annual fees demand math. Don’t keep a fee card unless the credits and benefits you actually use reliably exceed the fee after taxes and hassles.

Costs, Risks, and Fine Print to Watch

Rewards and HYSA yields only help if you keep costs down and avoid gotchas.

- Interest risk: Carrying a balance can swamp your rewards. Almost half of cardholders roll balances month to month, according to recent survey data—proof that a single missed payoff can undo months of careful optimization (Bankrate).

- Fee creep: Watch annual fees, foreign transaction fees, and balance transfer terms. “Deferred interest” promos can retrocharge interest if you don’t pay in full by the deadline.

- Redemption devaluation: Points can lose value, expire, or shift categories. Cash is simpler; if you prefer points, keep a calendar to redeem before expirations.

- Rate volatility: HYSA APYs are variable and respond to market moves and bank funding needs. The FDIC’s rate cap for savings (4.39% as of May 2026) also illustrates why extreme promos might be limited or conditional for some institutions (FDIC).

- Access and transfer limits: Many HYSAs allow easy ACH transfers, but some limit certain transaction types or enforce daily/monthly caps. If you need same-day cash, keep a buffer in checking.

- Insurance coverage: Confirm FDIC or NCUA insurance and the bank/credit union’s legal name (especially with fintechs that use a partner bank). Keep total deposits within insurance limits per institution.

- Data and privacy: Some cashback apps monetize your data. Read permissions; link only what’s needed; use two-factor authentication.

- Tax quirks: Purchase-linked card rewards are generally rebate-like (not income), but bank account bonuses and certain referrals can be taxable, potentially triggering 1099 forms (IRS).

Infographic — ‘How to rack up credit card rewards’ (illustrated guide to cash back, points, and strategies). — Source: Visualistan

Eligibility, Timing, and When Alternatives Make Sense

Eligibility: Rewards card approvals depend on issuer criteria (credit history, income, recent inquiries). New accounts can affect your average account age and available credit. HYSAs typically verify identity and may check consumer banking reports (e.g., ChexSystems). Some top APYs require direct deposit or minimum activity; if you won’t meet the conditions, choose a straightforward yield instead.

Timing: If your current savings rate is near the national average (0.38% in May 2026), moving to a competitive HYSA is a low-effort upgrade (FDIC). After that, quarterly check-ins are enough. Chasing every 0.05% APY bump can burn time and increase the odds of mistakes.

Alternatives for short-term cash: If you want rate certainty, consider a no-penalty CD or a short-term CD ladder; early withdrawal penalties vary. Very short-term treasuries can also be competitive and are backed by the U.S. government; they settle and mature on schedules that may not match emergency timelines, so ensure you have a liquid buffer in checking or HYSA. Always compare after-tax yields, liquidity needs, and any account requirements.

Red Flags

- “Up to” HYSA APY requires multiple hoops (monthly debit swipes, direct deposit, bill pays) you won’t reliably meet.

- Issuer defaults your autopay to “minimum due” rather than “statement balance.”

- Category caps so low that the headline percentage won’t move your annual totals.

- High annual fee card where your real, recurring benefits don’t exceed the fee.

- Rewards that expire quickly or can be redeemed only through low-value merchandise portals.

- Fintech savings product without clear FDIC/NCUA coverage or a named partner bank.

- Promos encouraging manufactured spend or prohibited activity to earn bonuses.

- HYSA terms with slow transfers, tight withdrawal limits, or hidden fees that make your emergency fund less accessible.

Frequently Asked Questions

Are cashback rewards taxable?

Generally, no—credit-card rewards tied directly to purchases are treated like rebates, not income, for consumers. An IRS Chief Counsel memo discusses this accounting view and timing for issuers. Exceptions include some bank account bonuses (often treated as interest) and certain referrals or unconditional sign-up payments, which may be taxable (IRS).

How many cards should I use?

For simplicity, one flat-rate cashback card is sufficient for most spending. If a single category card cleanly fits your routine (e.g., groceries), add it—then stop. More cards mean more complexity, more error risk, and higher odds of paying interest by mistake.

Is a HYSA safe?

A HYSA at an FDIC-insured bank (or NCUA-insured credit union) offers deposit insurance within legal limits. Confirm the institution’s name—especially with fintechs using partner banks—and keep total deposits within coverage caps.

What APY is reasonable right now?

As of May 2026, the national average savings APY was 0.38% (FDIC). Top online HYSAs often advertise 4%+ APY, and some promos, such as Varo’s 5.00% APY on up to $5,000 with requirements, have appeared in recent rate roundups (updates in early June 2026) (Bankrate). APYs are variable and can change.

Should I redeem for cash or travel?

Cash or statement credits are easiest and let you compound in your HYSA. Travel redemptions can be higher value, but they demand more tracking and are exposed to devaluations. Choose the path you will consistently execute without errors.

How often should I rate-shop my HYSA?

Quarterly is plenty. Move only for a meaningful, sustainable advantage after considering transfer speed, account requirements, and your time. The FDIC’s savings rate cap (4.39% in May 2026) helps explain why many offers cluster, limiting the practical spread (FDIC).

Can I automate moving cashback into savings?

Many issuers allow cashback redemption to a linked bank account. If not, take a statement credit, then set a recurring transfer from checking to HYSA for the same amount. The key is consistency—small, automatic moves add up without extra decisions.

0

0

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.