Can I create my own ETF? A practical guide

0

0

FinancePolice aims to clarify what a launch realistically requires so you can assess feasibility before speaking with counsel or service providers. Use the checklists and examples here as a starting point, then verify details with primary sources and prospective partners.

What it means to create an ETF: definition and quick context

An exchange traded fund is a pooled investment vehicle whose shares trade on an exchange like ordinary stock, while the fund itself holds a portfolio of assets that track an index or follow an active strategy. If you are asking how to start an etf, understanding this basic structure helps you see what you actually need to build: a legal issuer, a portfolio, and a way for shares to be created and redeemed on the market.

In the U.S., many ETFs operate under a standardized regulatory framework that removed the need for case-by-case exemptive orders for typical structures, meaning a familiar set of rules applies to many passive funds. The SEC’s Rule 6c-11 is the primary reference for that framework and explains how standard ETF exemptive relief is now implemented SEC Rule 6c-11 final rule. See also the SEC small entity compliance guide for additional implementation details.

Product design matters. A passive ETF that tracks a broad index, a transparent active ETF, and a non-transparent or novel strategy each follow a different practical and regulatory path. The choices you make at design stage materially change which approvals, partners, and operational systems you must arrange.

You can create an ETF if you assemble a sponsor and core service providers, secure seed capital (often from institutional market makers or authorized participants), meet exchange listing standards, and complete regulatory filings; feasibility and timeline depend heavily on product design and preparedness.

To put it simply: creating an ETF is not just about picking assets. It is about connecting a legal structure, service providers, capital, and exchange approvals so a traded share can exist and clear smoothly.

When considering whether to create an ETF, remember that the vehicle is distinct from mutual funds and private funds by how shares are created and redeemed and by the exchange listing and secondary market mechanics that make continuous pricing and intra-day trading possible.

Who is involved: sponsors, custodians, authorized participants and other core service providers

Launching an ETF requires coordinating organizations that together run the product day to day. The core parties are the sponsor or issuer, a custodian that holds the fund’s assets, a transfer agent or administrator that maintains shareholder records and NAV calculations, authorized participants who create and redeem shares, and a listing exchange where shares trade.

The sponsor or issuer is legally responsible for the fund, sets the strategy, and hires the other providers. The custodian safeguards securities and cash for the fund and works with settlement systems. The transfer agent records ownership and typically supports shareholder servicing and reporting. The administrator ensures NAV calculation, accounting, and other operational controls are in place.

Authorized participants, often market makers or institutional trading firms, play a dual role: they can provide initial seed capital to start the fund and they facilitate creation and redemption in the secondary market, which helps keep the ETF’s market price aligned with its underlying value. Industry guidance describes these participants as central to initial liquidity and ongoing exchange functionality ETF launch and seed capital overview.

Exchanges matter because they list the ETF and enforce listing standards, disclosure timelines, and trading rules. Nasdaq and NYSE Arca publish issuer guidance and listing steps specific to ETF listings, and their requirements shape what documents and controls sponsors must have in place before the first trade Nasdaq Listing Guide. The Nasdaq listing pdf guide is also available here.

In practice, a launch team commonly includes experienced counsel and operations specialists who coordinate among providers and the exchange. Building these relationships early helps avoid gaps in documentation, reduces onboarding delays, and gives practical clarity on expected timelines and costs.

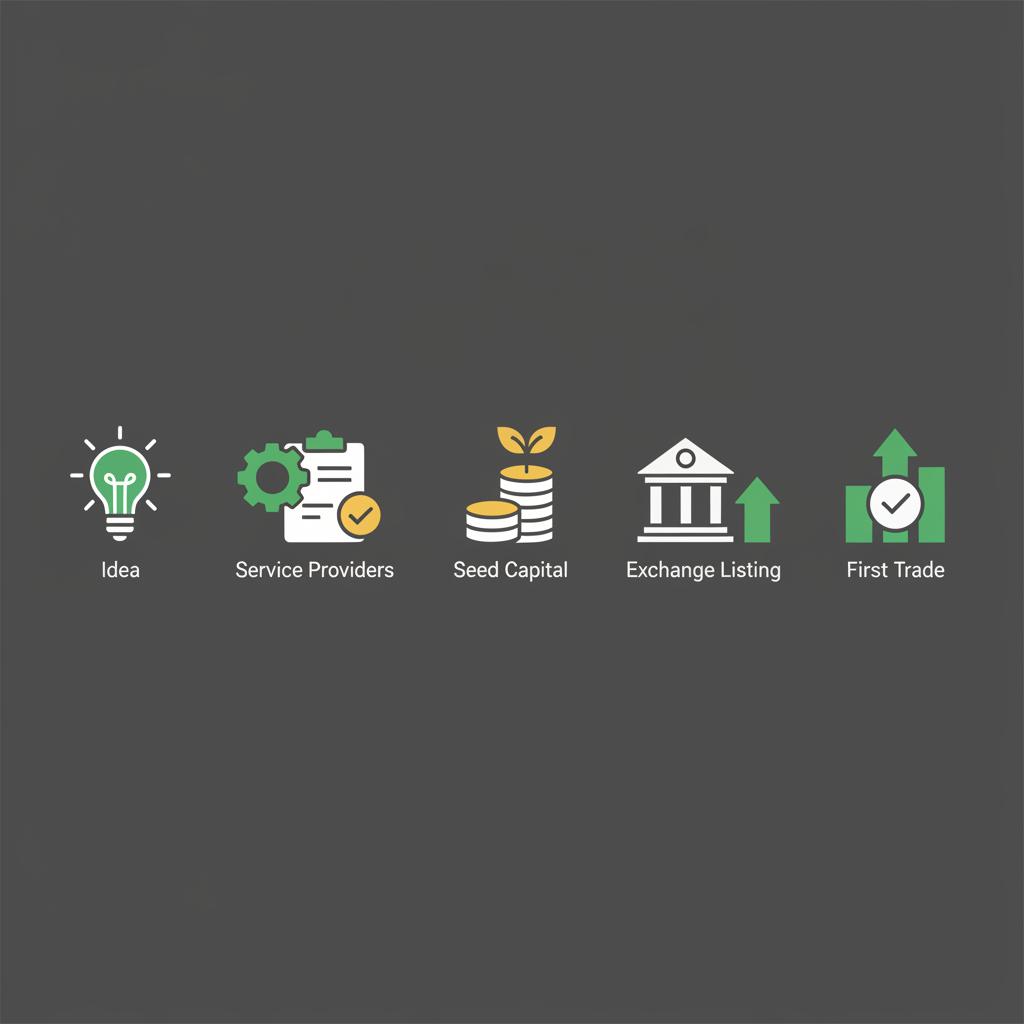

Step-by-step process to start an ETF: from product idea to first trade

Begin with product design. Define the investment strategy, index methodology if relevant, expected holdings, and whether the fund will be passive, transparent active, non-transparent active, or another model. The design choice affects later regulatory steps and operational complexity, so spend focused time on trade-offs before committing to a path.

Next, assemble service providers. Select a custodian, transfer agent/administrator, and identify potential authorized participants and market makers to discuss seed capital and liquidity plans. Early conversations with likely partners shorten later onboarding and help you understand what operational controls the exchange and counsel will expect.

Regulatory filings follow. For many standard ETF structures, Rule 6c-11 now provides the main framework and standardizes the exemptive relief that ETFs relied on before the rule, which simplifies the filings for common passive products SEC Rule 6c-11 final rule.

Check your readiness before you commit

Use the checklist later in this article to compare your team and capital readiness before you contact counsel or exchanges.

If your strategy is novel, involves non-transparent trading, or uses complex active management, additional regulatory coordination or bespoke agreements may be necessary. Those products can require more back-and-forth with counsel and, in some cases, extra disclosure or operational safeguards to satisfy exchange and SEC considerations ETF launch regulatory and timeline guidance.

After filing and internal readiness checks, you submit a listing application to an exchange. Exchanges like Nasdaq and NYSE Arca review the application, confirm listing standards are met, and coordinate the official listing date and ticker details. The exchange review is a practical gate that includes disclosure, trading rules, and readiness to support the securities at first trade NYSE Arca ETF listing guidance.

Operational setup and testing are the final steps before launch. This includes NAV and pricing systems, creation and redemption processes with authorized participants, transfer agent onboarding, and test trades where possible. Well-prepared passive ETFs can reach first trade faster; more complex products need deeper operational and compliance testing, which lengthens the schedule.

Practical timeline ranges vary. For a straightforward passive ETF, issuers and counsel report a compressed path that can be as short as a few months if all partners and documentation are ready. More complex or novel strategies typically take longer, commonly measured in many months up to a year or more, depending on regulatory needs and operational build-out Practical timeline guidance for ETF launches.

How product type changes what you must do: passive, active and novel ETFs

A standard passive ETF that tracks a public index usually follows the fastest, most standardized path. The index methodology and portfolio construction are typically transparent, the operational processes are well understood, and Rule 6c-11 covers many of the exemptive relief needs for these products, which simplifies filings and exchange review SEC Rule 6c-11 final rule.

Active ETFs can be relatively straightforward if they operate transparently and within familiar governance structures, but some active approaches, especially non-transparent or innovative execution models, require bespoke handling. Those approaches can trigger additional regulatory steps, special disclosures, or tailored agreements between the issuer and service providers to address investor protection and operational transparency concerns Law firm guidance on active and novel ETFs.

Non-transparent strategies, where the portfolio is not publicly disclosed intraday, tend to draw the most scrutiny because exchanges, market makers, and regulators focus on how liquidity and fair pricing will be maintained. When a product is novel in structure or transparency, expect extra documentation, possibly bespoke trading protocols, and longer coordination with counsel and the exchange.

Capital and seed funding: where the money comes from and what to expect

Seed capital and working capital are distinct. Seed capital is the initial portfolio funding that allows authorized participants to create shares that can trade publicly. Working capital and operational funding cover legal, compliance, service provider fees, and ongoing administrative costs until the fund reaches sustainable asset levels.

In practice, institutional market makers or authorized participants commonly provide seed capital for new ETFs. Industry reporting indicates institutional seed rounds remain the standard approach rather than relying on retail funding for initial liquidity and creation activity Seed capital and provider roles in ETF launches.

Seed needs vary with strategy. A simple, broad passive product typically needs smaller initial funding to establish tradable creation units and attract market makers. A niche or active product often needs more institutional backing to demonstrate liquidity and trading depth, which affects feasibility and timing.

Working capital is necessary to cover upfront professional fees like counsel and exchange filings, service provider onboarding, and initial operations. Those professional and operational costs matter, but many guides note they are frequently smaller than seed capital itself, which is often the dominant financial hurdle for first-time issuer teams ETF launch costs and capital overview.

Typical timelines and upfront costs: realistic schedule and major cost categories

Timelines reported by issuers and law firms commonly fall in a range from about three months for a well-prepared, simple passive ETF to six to twelve months or longer for active or novel strategies that require extra regulatory or operational work. The exact schedule depends on preparedness, complexity, and the speed of partner onboarding ETF launch timeline guidance.

Primary upfront cost categories include legal and compliance fees for filings and documentation, exchange listing fees and ongoing market data costs, and operational setup such as technology, NAV calculations, and service provider onboarding. Each of these categories can vary widely based on product complexity and the choices you make for providers.

Legal and compliance work often takes a disproportionate share of attention early because it shapes the filing package and disclosures the exchange will review. Experienced counsel can shorten the process by preparing standard templates and anticipating exchange questions, but that expertise is an upfront expense you should plan for.

Operational setup costs cover systems for NAV, portfolio accounting, reconciliation, and testing creation and redemption flows with authorized participants. These processes require staff time and vendor coordination, and deep operational readiness typically shortens exchange review time by reducing follow-up queries.

Common pitfalls and mistakes to avoid when launching an ETF

Underestimating seed or liquidity needs is a frequent error. Without sufficient seed capital and market maker interest, early trading can be thin, spreads can widen, and the fund may struggle to reach sustainable AUM, which can delay expected benefits and increase ongoing promotional effort.

Skipping early regulatory or exchange conversations for nonstandard strategies is another common problem. Novel or non-transparent products often require bespoke agreements or additional disclosures, and failing to anticipate these needs lengthens review and raises legal costs Active strategy regulatory considerations.

Compare provider readiness and timeline risks

Use monthly status updates for each item

Operational gaps are also common. Weak testing of creation and redemption flows, or late discovery of reporting mismatches between service providers, can cause last-minute fixes and delay listing. Early end-to-end testing with the actual providers reduces this risk.

Mitigation steps include early provider outreach, conservative capital planning that assumes higher seed needs for niche strategies, and working with counsel experienced in ETF launches to anticipate bespoke regulatory questions.

Practical examples and launch scenarios readers can relate to

Simple passive ETF scenario. Imagine a sponsor with a clear index license and a small team. They secure a custodian and transfer agent, find an authorized participant willing to seed a modest creation unit, and prepare filings aligned with Rule 6c-11. If documentation is complete and providers are ready, the path to first trade can be on the shorter side of the typical timeline.

Active or niche strategy scenario. Consider a fund with a less transparent active model. The sponsor must document trading protocols, address pricing and liquidity concerns, and may need additional disclosure or trading agreements. Those extra steps usually add to legal costs and extend the timeline because exchanges and counsel will review operational safeguards more closely. For readers looking for more detail on advanced ETF trading strategies, see advanced ETF trading strategies.

Checklist for a lean launch. Key items to compare are: clear product design and index methodology, committed authorized participant for seed, custodian and transfer agent chosen, seasoned counsel engaged, and an exchange list of required documents. Use this list to assess whether you have the minimal set of partners and capital to proceed.

Deciding next steps: checklist and how to know if launching an ETF is right for you

Decision checklist. Ask whether you have a viable product-market fit, access to institutional seed capital or committed authorized participants, a realistic operational team or vendor plan, and counsel experienced in ETF regulatory filings. If one or more of these is missing, consider alternatives before proceeding. You can also review related investing articles on our investing hub.

When to consult counsel and service providers. You should speak to experienced ETF counsel early if your strategy is active, non-transparent, or otherwise novel. Counsel and likely service providers can clarify exchange expectations, filing timelines, and documentation needs that materially affect feasibility.

Alternatives to starting your own ETF include partnering with an existing issuer that can act as the sponsor, licensing your strategy or index to a third party, or using other pooled vehicles where exchange listing is not required. These alternatives can reduce upfront capital needs and operational burden, though they involve trade-offs in control and economics. For related guidance on maximizing outcomes, see our guide on maximizing your portfolio returns.

A well-prepared passive ETF with a clear index, committed service providers, and seed support from an authorized participant can reach first trade in a shortened timeline, often a few months if all documentation and partners are ready.

Seed capital is commonly provided by institutional market makers or authorized participants rather than retail investors; sponsors typically arrange institutional backing to ensure liquidity and creation unit funding.

For many standard ETFs, SEC Rule 6c-11 standardizes exemptive relief and reduces the need for bespoke orders, but novel or non-transparent strategies may still require additional regulatory coordination.

If you lack a committed authorized participant or institutional seed backer, explore partnerships with existing issuers or alternative vehicles before attempting a standalone launch.

References

- https://www.sec.gov/rules/final/2019/33-10612.pdf

- https://www.etf.com/what-it-takes-to-start-an-etf

- https://listingcenter.nasdaq.com/

- https://www.sec.gov/investment/exchange-traded-funds-small-entity-compliance-guide

- https://listingcenter.nasdaq.com/assets/ETP_Listing_Guide.pdf

- https://www.ici.org/faqs/faqs_etfs

- https://www.nyse.com/markets/nyse-arca

- https://www.goodwinlaw.com/insights/launching-an-etf

- https://financepolice.com/advertise/

- https://financepolice.com/advanced-etf-trading-strategies/

- https://financepolice.com/category/investing/

- https://financepolice.com/maximize-your-portfolio-returns-with-tax-efficient-investing-strategies-for-2026-and-future-years/

0

0

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.

0

0

0

0