LNG markets at risk? Rystad warns of Hormuz-driven price spike

0

0

Spot liquefied natural gas (LNG) prices are expected to spike in 2026 due to the halt in shipping activities through the Strait of Hormuz, Rystad Energy said.

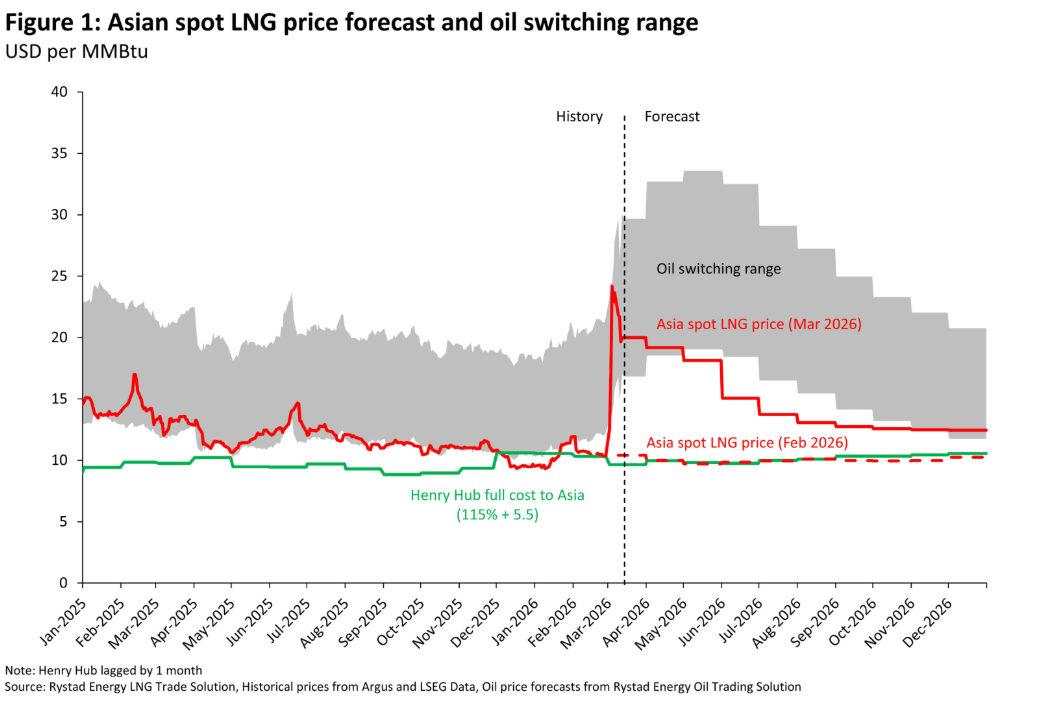

“Rystad Energy’s view is that Asian spot LNG prices in 2026 will rise from around $10 per MMBtu pre-conflict to about $14 per MMBtu,” Kaushal Ramesh, vice president, gas & LNG research, said in an emailed commentary to Invezz.

LNG production from Qatar and the United Arab Emirates is only likely to return to full capacity by the second half of May as shipping is expected to remain truncated through early April, according to Rystad Energy.

Rystad’s revised forecast concentrates on Asian spot prices, rather than the Dutch TTF (Title Transfer Facility), because Middle Eastern LNG supply disruptions have redirected price setting to Asia.

This shift is significant as over 85% of Qatar's and the UAE's LNG was delivered to Asia in 2025.

“Europe is expected to require an additional 18 million tonnes of LNG year-on-year in 2026, meaning TTF prices will largely be determined by a no-arbitrage condition,” Ramesh said in the commentary.

Before the conflict, Rystad’s expectation for 2026 was generally a state of balance, with spot prices approximating the long-run marginal cost of US LNG.

“The current price environment is likely to persist as long as the Strait of Hormuz remains closed, with additional upside if oil prices rise further.”

Gulf risks cloud LNG supply

Before the Iran conflict, the anticipated growth in LNG supply was substantial, exceeding 30 Mt year-on-year, primarily fueled by contributions from the US, Canada, and Australia.

However, accounting for the estimated loss of approximately 11 Mt from Qatari and UAE volumes throughout our base case period, the net projected growth in LNG production remains above 25 Mt, according to the Norway-based energy intelligence company.

It is important to note that this projection currently assumes uninterrupted supply from Omani LNG.

Nonetheless, Omani supply could face risks, particularly since Iran's attack on Sohar has led some LNG buyers to avoid the region altogether, the agency said.

Asia LNG demand softens

The primary decrease in LNG demand is anticipated in emerging Asia, according to Rystad.

However, the worst-case scenario only necessitates slowing the growth of LNG demand, not an actual reduction from 2025 figures, which softens the overall effect.

Furthermore, approximately 900,000 tonnes of Intra-Gulf LNG imports are affected because Qatari LNG is blocked from reaching Kuwait, and external supplies cannot transit the Strait of Hormuz.

“Demand reduction may be split across markets outside of emerging Asia that might have flexibility, such as through coal-fired power and demand-side management measures,” Rystad added.

What could a six-month disruption be like?

An alternative, more severe scenario involves the Strait remaining closed for six months as the conflict persists, with a full reopening anticipated by September.

Damage to the LNG production facilities at Ras Laffan or Das Island could also lead to this scenario.

“This would take approximately 40 Mt of LNG production off the market and would need curtailment even from price-inelastic demand in Europe and OECD Asia,” Rystad noted.

“TTF and Asian spot prices would follow oil higher to the vicinity of $30 per MMBtu for the year, as prices signal switching to heavy oil fuels. Still not as high as 2022, but close.”

The $30 per MMBtu figure for 2026 is based on a potential six-month disruption, with the acknowledgement that daily figures could be significantly higher than the quoted yearly average, the agency said.

Lessons for future

The frequent discussions surrounding a potential disruption of the Strait of Hormuz have become a reality, with an unexpected escalation in Iranian military action.

This includes attacks on Gulf nations like Qatar, a country with whom Iran previously maintained friendly relations.

“Geostrategic sources of LNG supply that can reach their energy-security focused demand markets without travelling through chokepoints or current or potential disputed territory will fetch a reliability premium,” according to Rystad.

A quick resolution is in the long-term interest of the LNG industry.

The situation should be framed as a 'precautionary disruption' with a swift return to normal, rather than a prolonged conflict-zone outage.

A six-month disruption scenario poses a significant risk.

It could hurt long-term LNG demand in emerging markets, leading to even lower prices in the early 2030s once the post-2022 wave of LNG projects is fully operational.

Furthermore, energy security-focused markets may revise their procurement strategies to reduce dependence on the Middle East, the agency added.

In response, Middle Eastern LNG producers may intensify their efforts to develop supply sources in other regions, including those targeting the APAC market.

“The markets most exposed to this disruption are in South Asia, which limits how far prices can rise compared with 2022, when Europe faced a more severe energy security shock,” Ramesh said.

The post LNG markets at risk? Rystad warns of Hormuz-driven price spike appeared first on Invezz

0

0

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.

0

0

0

0

0

0

0

0