US oilfield services set for rapid growth; Rystad sees 30-40 rigs

0

0

As the global energy crisis continues amid persistent disruption in the Strait of Hormuz, US shale producers, currently exercising caution, may soon accelerate activity to boost output before the inevitable escalation of service prices, Rystad Energy said.

US oil exploration and production (E&P) companies have recently shown the first public signs of increasing activity in response to higher prices.

“More may follow, especially as the disconnect between physical and financial markets for oil begins to reverberate through the forward curve,” head of North America oil and gas research, Jai Singh at Rystad Energy, said in an analysis.

Caution is warranted as market participants look to adjust their strategies, given the potential for rapid changes in oil prices following the tentative reopening of the Strait of Hormuz.

Shifting strategies

If momentum behind activity addition becomes clear, the ‘wait and see’ logic could turn quickly to one of ‘don’t miss the boat’ on service costs.

Initially, E&Ps maintained capital discipline and unchanged plans despite war-driven price volatility.

As Strait of Hormuz volume disruption grew, producers adopted a 'wait and see' approach, prioritising hedging and cash harvesting over increased activity.

Steep backwardation and lower drilled-but-uncompleted (DUC) inventories disincentivise adding rigs and prevent immediate production spikes to capitalise on $100 West Texas Intermediate crude oil.

With the forward curve failing to incorporate the full impact of the supply disruption, suggesting that prices will remain elevated for an extended period, some producers are now considering increasing the number of active rigs.

The temporary ceasefire announcement has introduced uncertainty, leading to increased caution and likely putting further announcements on hold.

“Even if the war ends and the Strait of Hormuz gradually reopens, geopolitical premiums, stockpiling demand and a new transit regime in the strait may keep prices higher for longer,” Rystad Energy said in the analysis.

This will likely still create a supportive price environment for shale activity additions during this year.

Service price escalation

The oilfield service sector is poised for rapid expansion, reminiscent of the widespread inflation and focus on the availability of super-spec drilling rigs and E-Fleet term commitments seen in 2021.

Current market pricing suggests an anticipated addition of approximately 30 to 40 rigs and between eight and 12 frac fleets before the close of the year.

Rystad Energy’s view is that this will go hand in hand with around 6% drilling and completion inflation in aggregate.

“We anticipate the back-end of the futures curve will rise in 2027 and 2028 oil prices as Middle Eastern supply disruption drags on,” the agency said.

If WTI crude oil prices remain sustained in the $85 to $90 per barrel range, inflation for the same set of drilling and completion categories is projected to be between 18% and 20%, the agency added.

The most significant price increases are anticipated in land rigs (18% to 20%), oil-country tubular goods (20%), frac services (18% to 25%), and fuel (20% to 25%).

Similar to 2021, an estimated 82 to 110 rigs are practically deployable, with varied capital needs, the analysis showed.

Day rates will increase as more rigs are added.

The first 15–25 rigs require almost no capital, while the final 25 will need millions for upgrades, according to the agency.

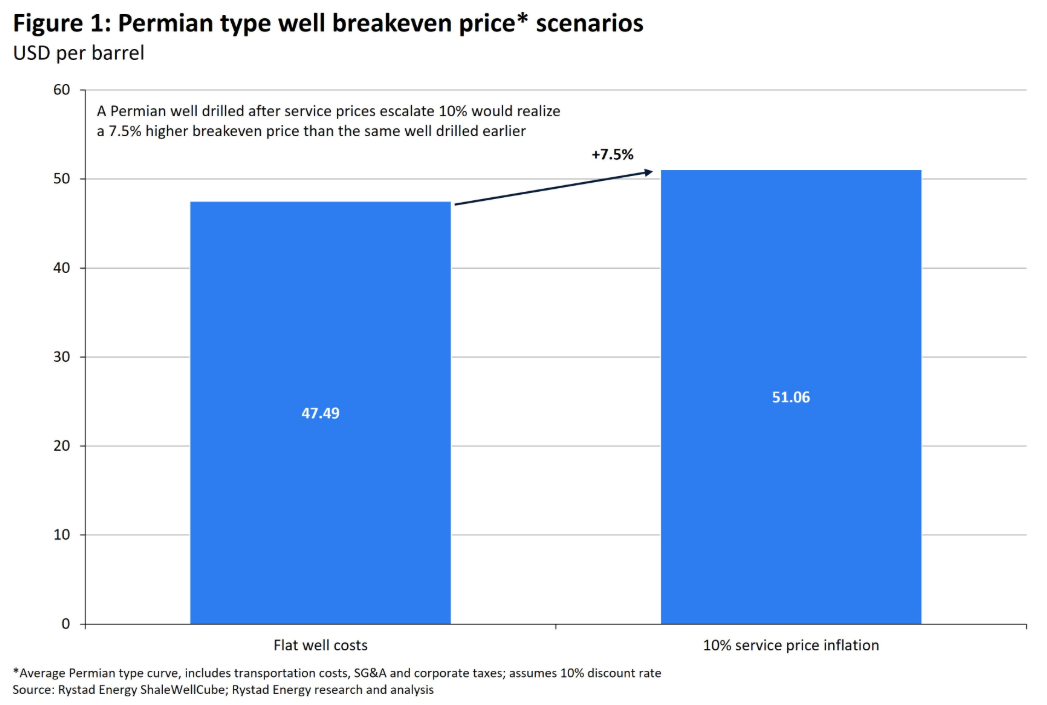

Breakeven prices and benefits

Rystad analysed a typical Permian well to estimate the general effect of postponing the action, rather than implementing it immediately.

A 10% increase in well costs raises the well's breakeven price by $3.57 per barrel, according to the analysis.

This cost escalation is also clearly demonstrated by comparing the Internal Rates of Return (IRRs) of the two wells.

The well with the lower cost yields an IRR of 104%, which is 40 percentage points higher than the 63% IRR of the higher-cost well.

Even though both wells would still be commercially viable, particularly given the current pricing, delaying the reactivation of a rig could hinder an operator's ability to capitalise on higher oil prices.

“Early actors will reap superior margins once their wells enter production a few months down the line,” Singh said.

We find that for an average Permian Basin well, a 10% higher drilling and completion cost for a new well correlates to a 7.5% higher breakeven price and 40% lower internal rate of return (IRR) over the well’s lifetime than the same well drilled prior to cost escalation.

The post US oilfield services set for rapid growth; Rystad sees 30-40 rigs appeared first on Invezz

0

0

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.

0

0

0

0

0

0

0

0