FBI Advises To Steer Clear Of Crypto Money Transmitting Services That Don’t Comply With KYC

9d ago•

bullish:

0

bearish:

0

Share

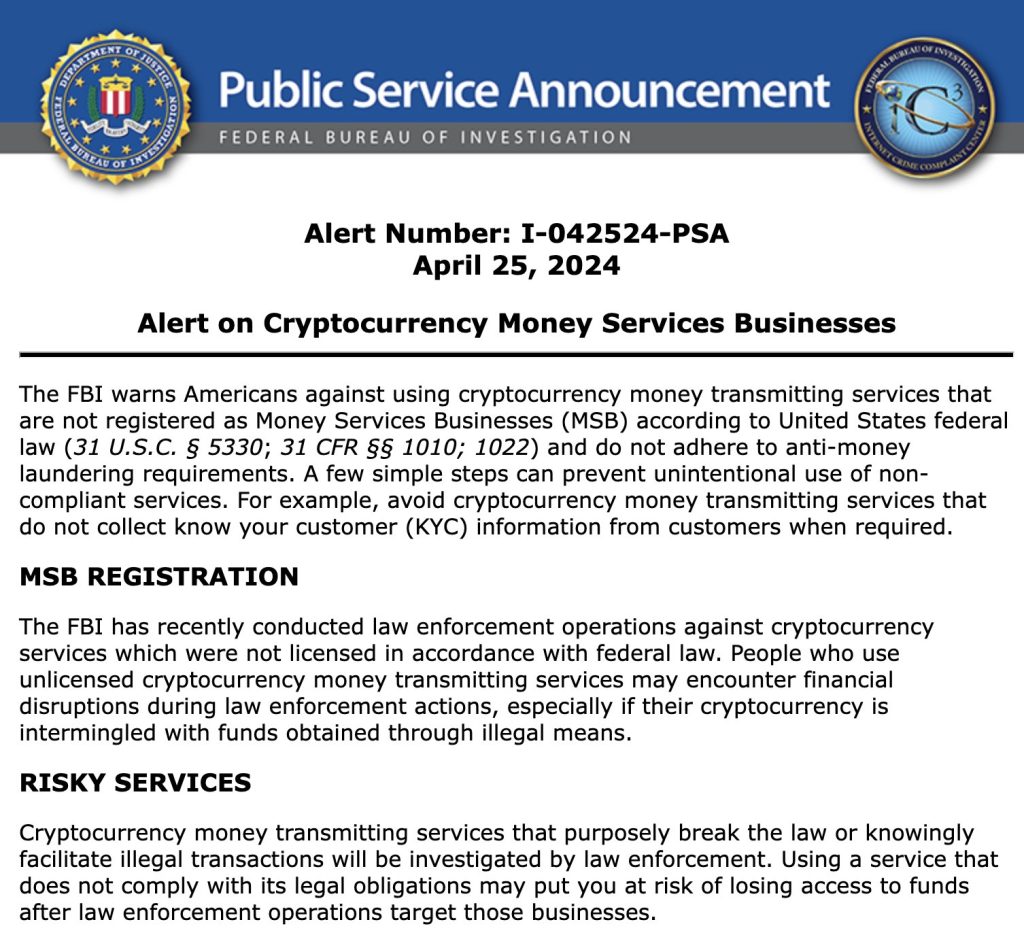

Today (April 25), the FBI released a public service announcement, designated as Alert Number I-042524-PSA, cautioning Americans about the risks associated with using cryptocurrency money transmitting services that are unregistered and do not adhere to Know Your Customer (KYC) standards.

The announcement emphasizes the importance of only transacting with registered Money Services Businesses (MSBs) that comply with anti-money laundering (AML) regulations, highlighting the agency’s commitment to safeguarding financial transactions in the digital currency space.

FBI Says Failure To Comply May Result In Financial Disruptions During Law Enforcement Actions

Under United States federal law, cryptocurrency money transmitting services are required to register as Money Services Businesses (MSBs) and comply with Anti-Money Laundering (AML) standards. The Federal Bureau of Investigation (FBI) has issued a warning that non-compliance can lead to significant financial disruptions, especially when funds are intertwined with money obtained through illegal means.

The FBI further emphasized that any services found to be facilitating illegal transactions or breaching federal regulations are liable for investigation by law enforcement authorities. Users of such services risk losing access to their funds during enforcement actions. This advisory comes in the wake of recent legal actions taken by the U.S. Department of Justice (DOJ). Just yesterday, the DOJ apprehended the founders and CEO of Samourai Wallet, a well-known privacy-centric Bitcoin wallet and mixer. They were accused of laundering over $100 million derived from criminal activities.

Collaborating with law enforcement agencies in Portugal and Iceland, the DOJ arrested one of the founders and executed seizures of Samourai’s web servers, domain, and issued a seizure warrant for the application on the Google Play Store.

FBI Says That Just A Few Steps Can Avoid Bigger Problems

In the FBI release, the institution emphasized the importance of avoiding cryptocurrency money transmitting services that fail to collect mandatory Know Your Customer (KYC) information. KYC protocols typically require details such as name, date of birth, and address from customers to ensure compliance with regulatory standards.

Additionally, the FBI advises individuals to verify whether a business is registered as a Money Services Business (MSB) using a tool provided by the U.S. Financial Crimes Enforcement Network (FinCEN). An examination conducted using this tool confirmed that reputable crypto firms, including Coinbase and Kraken (officially recognized as Payward Financial Inc), are indeed registered as MSBs, highlighting their compliance with regulatory expectations.

How Criminals Exploit KYC Loopholes

RelyComply, the AML platform, has identified that criminals consistently exploit vulnerabilities in Know Your Customer (KYC) processes, particularly in sectors like fintech, cryptocurrency, and payments. These industries are particularly susceptible due to the appealing “super-fast” digital onboarding processes that often come with minimal checks.

Such procedures not only attract legitimate customers but also provide an easy gateway for criminals who use forged or stolen identity documents to quickly open multiple accounts. These accounts, often referred to as “money mule accounts,” then become channels for laundering illicit funds through what appear to be legitimate transactions.

Furthermore, shared KYC utilities, which are popular due to their high customer pass rates, are prime targets for exploitation. Criminals take advantage of these systems, which typically involve a single-time verification process. By bypassing these checks, they can create accounts at multiple financial institutions using synthetic identities or manipulated biometrics. This reliance on shared KYC data, coupled with a lack of robust verification and continuous monitoring, exposes firms to regulatory penalties and reputational risks.

Additionally, dormant accounts that have passed initial KYC checks pose another vulnerability. Criminals acquire these accounts, often through purchases on dark web marketplaces, and reactivate them to channel dirty money. The ease of updating account information and reactivating them allows criminals to evade the more rigorous scrutiny normally applied to new accounts, further facilitating the discreet integration of illicit funds into the financial system.

Regulatory Frameworks Are Always Behind Criminals’ Technological Edge

The challenges of combating money laundering are compounded by third-party KYC requirements, which are often less stringent and susceptible to exploitation. Criminals utilize sham companies or recruit money mules to exploit these weaknesses in the KYC process, thereby undermining the broader financial integrity.

Sophisticated obfuscation techniques pose significant hurdles even for robust KYC systems. Launderers employ various tactics such as smurfing, trade-based laundering, and the use of complex corporate structures to obscure the origins of their funds. These methods make it increasingly difficult to trace the illicit money and prosecute those responsible.

In the digital age, a new form of money laundering has emerged, known as cyber laundering. Criminals take advantage of online tools, including cryptocurrency tumblers and virtual asset trades, to anonymously move illicit proceeds. Despite the increasing prevalence of these digital laundering methods, regulatory frameworks remain outdated, thereby granting criminals a technological advantage.

A notable example of this exploitation occurred at Banxso, where the criminal group Immediate Matrix used advanced technologies like deepfakes to evade detection and execute scams. Although Banxso was not directly involved in the misconduct, the sophisticated nature of these scams inflicted significant reputational damage on the platform, highlighting the ongoing challenges in the financial sector.

The post FBI Advises To Steer Clear Of Crypto Money Transmitting Services That Don’t Comply With KYC appeared first on Coinfomania.

9d ago•

bullish:

0

bearish:

0

Share

Manage all your crypto, NFT and DeFi from one place

Manage all your crypto, NFT and DeFi from one placeSecurely connect the portfolio you’re using to start.

bullish:

0

bearish:

0

bullish:

0

bearish:

0